The Other Billion Patients

Why the country with the planet's largest animal population is one of its smallest medicine markets, and what to make of the four listed names everyone calls "animal pharma."

If you would like to watch a video I made on this topic:

Hello friends,

Let’s begin this one with a question.

When you think about “healthcare” in India as an investing theme, you picture hospitals, diagnostics chains, the big formulation exporters, maybe a CDMO or two. Human patients. People in waiting rooms.

You almost certainly do not picture a buffalo.

Which is strange, because India has roughly 535 million heads of livestock, the largest cattle and buffalo population on earth, the largest milk output of any country, one of the largest poultry flocks going, and a companion-animal population that is exploding as urban India discovers the joy and the vet bills of owning a labrador. Add it up and you are looking at well over a billion animals. A billion-plus patients who get sick, need vaccinating, throw up after eating something they shouldn’t, and occasionally need an antibiotic.

And here is the number that frames this entire piece. Despite owning the world’s largest animal population, India accounts for roughly 3% of global animal-health spending. The country that has the most animals spends almost the least, per animal, keeping them healthy.

That gap is the thesis. It is the same shape as the per-capita-electricity gap that anchored my power piece, or the fibreisation gap in the optical fibre piece. A large, structurally underserved base, a known direction of travel, and a decade of catch-up spending that most investors have not bothered to model because, frankly, animal medicine is unglamorous. Nobody posts about deworming tablets on FinTwit.

This piece is about that unglamorous, under-penetrated, quietly compounding market. It is about the value chain that produces veterinary medicine, where the real money and the real moats sit on that chain, the tailwinds turning a sleepy sector loud, and four Indian listed companies that occupy very different rungs of the ladder.

If you want the elevator pitch first, here it is.

The structural opportunity in Indian animal health is real and genuinely under-penetrated. But of the four names retail investors most often lump together as “animal pharma plays,” only two are actually pure animal-health businesses. The largest and most famous of the four has just merged into something that is now half human-pharma. The cheapest-sounding one is really a human formulations exporter with a veterinary side-arm. The gap between the apparent animal-health basket and the real one is wider than the tickers suggest, and that gap is where the mispricing lives.

Part 1: The Other Billion Patients

Start with the size of the prize, because the range of published estimates is wide enough to be useless if you don’t reconcile them.

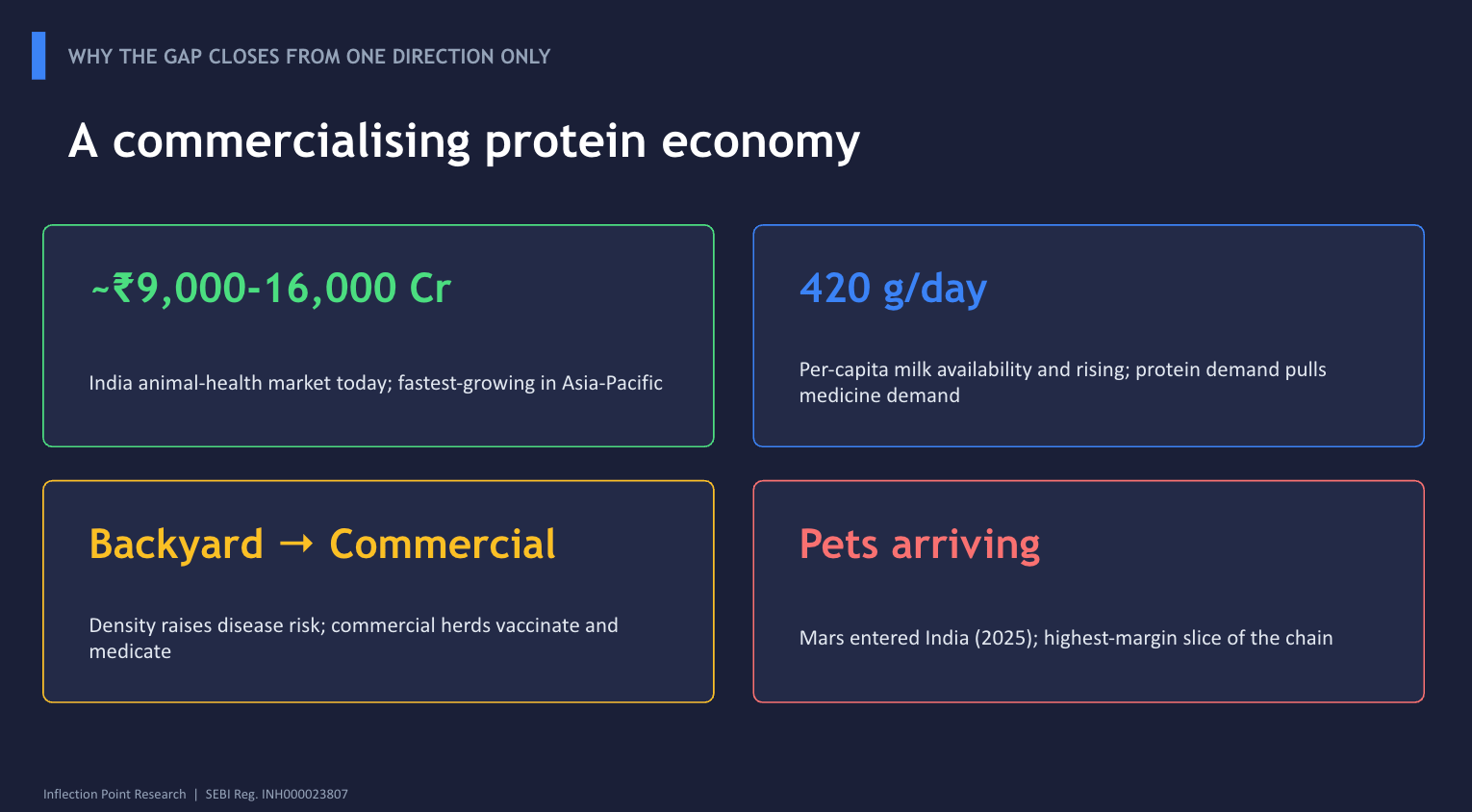

Depending on whose report you read, the Indian animal-health market is worth somewhere between roughly ₹9,000 crore and ₹16,000 crore today, with forecast growth rates clustering in two camps: a conservative 7% or so (the rupee-denominated, livestock-heavy view) and an aggressive 13 to 14% (the dollar-denominated, companion-animal-and-diagnostics-led view). Grand View pegs India at about USD 2 billion in 2024, growing near 14% to USD 4.2 billion by 2030. IMARC sees a steadier 7% climb. The truth is almost certainly that the commodity livestock segment grows in the high single digits while companion animals and diagnostics grow in the mid-teens, and the blended number lands somewhere in between.

The exact figure matters less than the shape, and the shape is unambiguous. India is the fastest-growing animal-health market in Asia Pacific, off a small base, and it accounts for only about 3% of global spend despite a far larger share of the world’s animals. The global animal-health market (pharmaceuticals, vaccines and feed additives, the product layer rather than the broader vet-services definition) is roughly USD 40 to 45 billion. India is a rounding error in it. That is the penetration gap, and it closes from one direction only.

Why does it close? Because the inputs that drive animal-medicine demand are all moving the right way at once.

India’s livestock is no longer mostly a backyard affair. The structural shift is from subsistence rearing toward commercial dairy, organised poultry, and increasingly aquaculture and piggery. Commercialisation means density, density means disease risk, and disease risk in a commercial herd or a 50,000-bird poultry shed is not something you treat casually: you vaccinate prophylactically, and you medicate at the first sign of trouble, because the alternative is losing the flock. A backyard farmer with three desi hens spends nothing on animal health. A commercial integrator with a million birds spends meaningfully, per bird, every cycle. India is moving, slowly but unmistakably, from the first model to the second.

Layer on protein consumption. India’s per-capita milk availability is now around 420 grams a day and rising; egg and poultry-meat consumption are growing faster than almost any food category. Every incremental litre of milk and every incremental kilo of chicken is produced by an animal that needs to stay healthy and productive to be economic. Animal health is, quite literally, an input cost into the protein economy, and the protein economy is one of the most reliable secular growth stories in the country.

Then there is the companion-animal wave, which is where the margins get interesting. Urban pet ownership is rising fast, pet humanisation (treating the dog as a family member with a family member’s medical budget) is following the global script, and global capital has noticed. In February 2025, Mars, the world’s largest veterinary-clinic owner, entered India by taking a stake in a local vet-clinic business. Pet insurance is nearly non-existent today, which is precisely the kind of zero-base that turns into a growth vector. Companion-animal medicine carries richer margins than livestock because the buyer is an emotional human, not a cost-accounting farmer.

This is the demand floor. Now, the value chain, because where on it you stand determines almost everything about the economics.

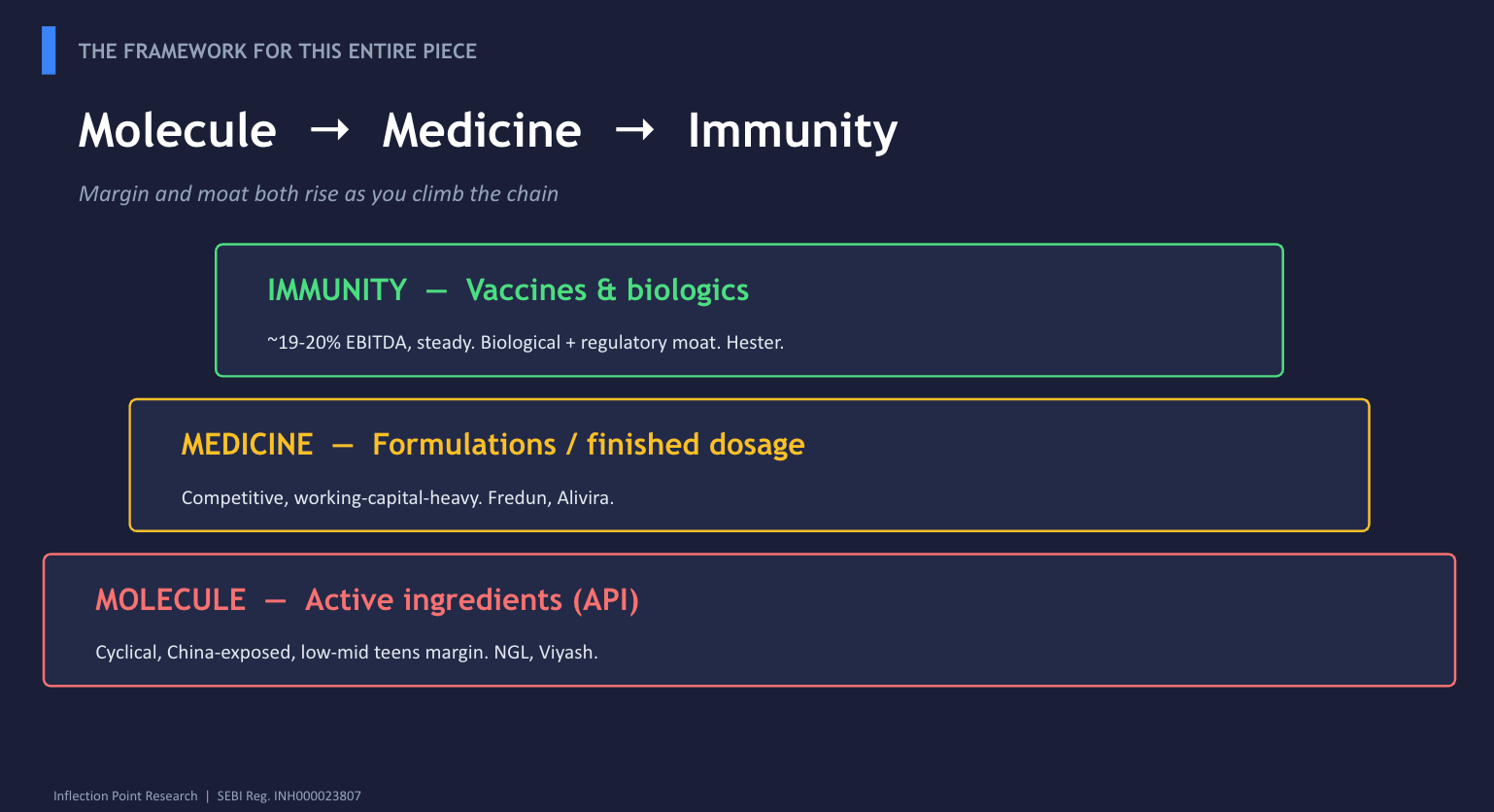

Part 2: Molecule, Medicine, Immunity

The animal-pharma value chain has, broadly, three productive layers and a distribution layer on top. The single most important thing to understand is that margin and moat both rise as you climb. Getting the layer right matters as much as getting the company right.

Layer 1: The Molecule (active pharmaceutical ingredients and intermediates). This is the chemistry. Somebody has to synthesise the actual drug substance: the anthelmintic that kills the worm, the antibiotic, the anti-parasitic, the anti-inflammatory. Veterinary APIs are made in chemical reactors, sold by the tonne, and priced against global competition, overwhelmingly from China. The economics are those of a specialty-chemicals business with a pharma label: cyclical, exposed to raw-material and realisation swings, and vulnerable to Chinese oversupply. When China floods a molecule, prices crater and Indian API makers’ margins compress hard. EBITDA margins here run in the low-to-mid teens in good times and can halve in bad ones. This is the layer where NGL Fine Chem lives, and where the merged Viyash also makes a large part of its money.

Layer 2: The Medicine (formulations and finished dosage forms). The molecule on its own treats nothing. It has to be turned into a tablet, a bolus, an injectable, a syrup, a premix, or a pour-on. This is the formulations layer, closer to the customer, branded or generic, sold across geographies. Margins are a touch steadier than pure API because there is product differentiation, registration barriers, and customer stickiness, but in commodity generics, it is still a competitive, working-capital-heavy grind. Fredun plays here (mostly for humans, partly for animals), Viyash’s Alivira brand plays here for animals, and NGL is inching forward into it.

Layer 3: Immunity (vaccines and biologics). This is the fortress. Animal vaccines are not chemistry; they are biology: live and inactivated viral and bacterial vaccines grown on eggs, cell lines, and in fermenters, under sterile conditions, in facilities that can take years and serious capital to build and qualify. A poultry vaccine maker needs biosafety-level containment, regulatory licences per product, and a cold-chain distribution network. New entrants cannot simply rent a reactor and undercut you. The qualification cycles are long, the regulatory moat is real, and as a result, vaccine economics are both higher-margin and far more stable than API economics. This is where Hester Biosciences sits, alone among our four, and it is no accident that Hester runs structurally higher and steadier EBITDA margins than the three drug-makers.

The distribution and brand layer on top. Whoever controls the relationship with the farmer, the integrator, the vet, and increasingly the pet parent, captures a durable slice of value through branded health products, feed supplements, and services. Hester has this in poultry; the formulation players build it through field forces and distributor networks.

Notice the funnel, and notice that it is the same shape I keep drawing in these pieces. At the molecule layer, you compete with China on price. At the medicine layer, you compete on registrations and reach. At the immunity layer, you compete with a handful of qualified biological manufacturers and the barrier to entry is a moat, not a hurdle. The further up you go, the fewer the competitors and the more durable the margin. If you want the structural rent of this sector rather than the cyclical scraps, you want to be long the top of the chain, or at least to know precisely which rung you are buying.

Part 3: Why This Is Suddenly Worth Your Attention

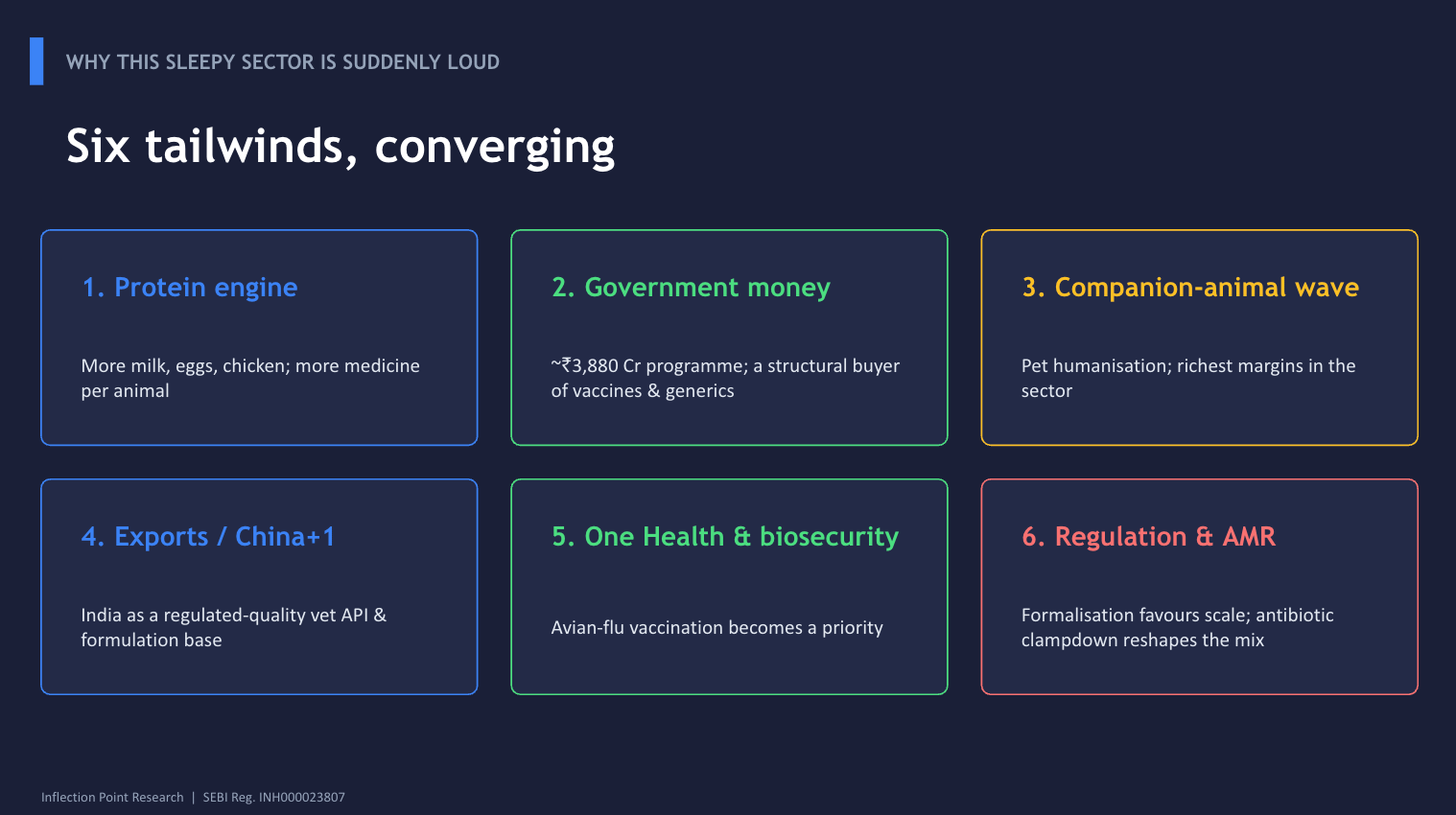

Six tailwinds are converging. Individually, each is a reason to look. Together, they are the reason this sector is finally getting a re-rating conversation.

One: the protein and commercialisation engine, covered above. More milk, more eggs, more chicken, more density, more medicine per animal. The base case for the sector needs nothing more than this to work.

Two: government money and government mandates. This is the part most equity investors under-weight. In March 2025 the Union Cabinet approved a revamped Livestock Health and Disease Control Programme with a budget of about ₹3,880 crore for FY25 and FY26. It has three arms: the National Animal Disease Control Programme (mass vaccination drives against foot-and-mouth disease, PPR or “goat plague,” and brucellosis, with eradication targets stretching to 2030), the broader Livestock Health and Disease Control component, and a brand-new Pashu Aushadhi initiative to distribute affordable generic veterinary medicines through PM-Kisan Samriddhi Kendras and cooperatives. Translation: the government is now a structural, recurring buyer of vaccines and generic veterinary drugs at national scale. The companies positioned to supply those tenders have a demand vector that did not exist at this size a decade ago.

Three: the companion-animal and pet-humanisation wave. Mars’s entry, the nascent pet-insurance market, and the premiumisation of pet care in metros. This is the highest-margin slice of the sector, and it is growing fastest.

Four: exports and the China-plus-one logic. India is becoming a credible low-cost, regulated-quality manufacturing base for veterinary APIs and formulations, exporting to Africa, Latin America, Southeast Asia, the CIS region, and increasingly the regulated US and EU markets. Every one of our four companies has a meaningful export story. The same China-plus-one tailwind that lifted human-pharma APIs and specialty chemicals is now reaching their veterinary cousins, with the added kicker that global innovators are looking to outsource animal-health R&D and manufacturing.

Five: One Health and zoonosis awareness. Post-Covid, the recognition that animal, human, and environmental health are one interconnected system has moved from conference slideware to policy. Avian influenza outbreaks, in particular, have made poultry vaccination a biosecurity priority, not just a productivity one. India approved H9N2 poultry vaccines and tightened farm biosecurity through 2025 and 2026.

Six, and this one cuts both ways: regulation and antimicrobial resistance. From January 2025, the Central Drugs Standard Control Organisation made online submission mandatory for all veterinary drug applications, formalising and tightening a previously loose market. Formalisation favours the compliant, scaled players and squeezes the grey-market fringe, which is a tailwind for our names. But the flip side is that the global clampdown on antibiotic use in food animals (to slow antimicrobial resistance) is a structural headwind for anyone over-indexed to veterinary antibiotics, and a tailwind for vaccines, gut-health products, and alternatives. Which molecules and products a company sells matters more than it used to.

Put the six together and you have the most supportive backdrop Indian animal health has had in this century. The question, as always, is who actually captures it, and at what price you are being asked to pay for the privilege.

Part 4: The Label Problem

Here is where I have to spoil the neat story, because rigour demands it and because this is precisely the variant-perception edge in this sector.

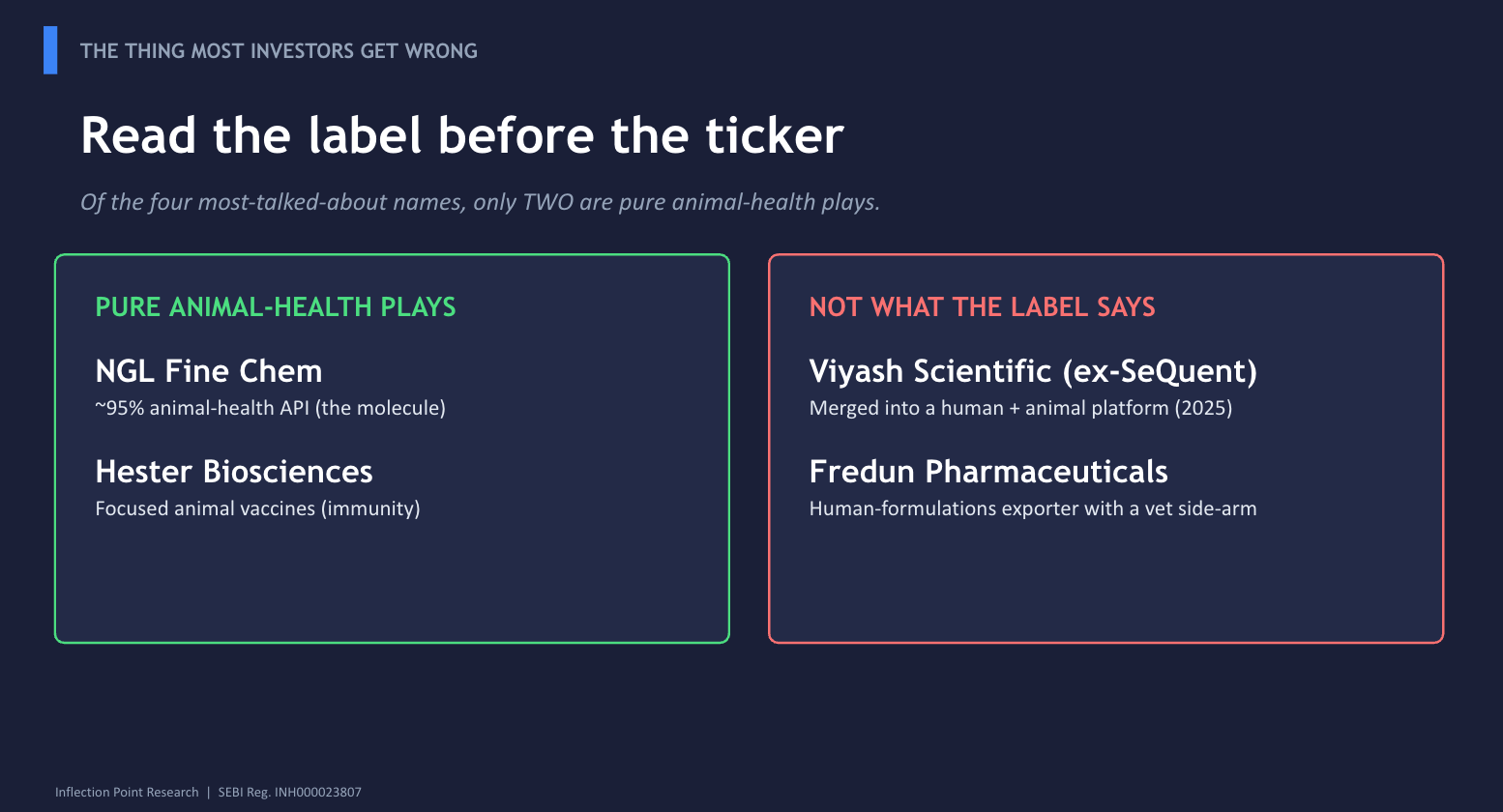

If you ask most retail investors for the listed Indian animal-pharma names, the four that come up most often are the four in this piece: NGL Fine Chem, Viyash Scientific (the company formerly and famously known as SeQuent Scientific), Fredun Pharmaceuticals, and Hester Biosciences. Treated as a basket, they look like a clean way to play the theme.

They are not a clean basket. Of the four, only two are pure animal-health businesses.

NGL Fine Chem is the real thing on the molecule layer: roughly 95% of its revenue is animal-health API. A genuine pure-play.

Hester Biosciences is the real thing on the immunity layer: a focused animal-vaccine and animal-health-products company, no human business to speak of. The purest play of the four in business terms.

Viyash Scientific is the twist. Until late 2025, this was SeQuent Scientific, the single largest and most credible pure-play animal-health company India had, the Carlyle-backed champion of the whole sector. Then, in November 2025, Carlyle merged its privately held human-API platform, Viyash Life Sciences, into SeQuent and renamed the combined entity Viyash Scientific. The merged company is now a human-plus-animal API, formulations and CDMO platform. A senior analyst quoted at the time of the announcement put it bluntly: the deal would not move the Indian animal-health industry, because Viyash makes human APIs. The most famous “animal-pharma stock” in the country is now, by revenue and by growth engine, substantially a human-pharma company. The animal-health business (the Alivira brand) is still there, still global, still real, but it is no longer the whole story or even the majority of it.

Fredun Pharmaceuticals is the other twist. Fredun is, at its core, a human-formulations exporter: antihypertensives, antidiabetics, antiretrovirals, narcotics, nutraceuticals, shipped to 90-odd countries. It has an animal-healthcare arm, but a chunk of that animal-health activity sits in group entities (Fredun Healthcare and Fredna Enterprises) rather than fully inside the listed company, and animal health is one of several diversification arms, not the engine. Buying Fredun as an “animal-pharma play” is a little like buying Finolex Cables as an “optical-fibre play,” a mistake I spent two thousand words on last month. The label and the business have drifted apart.

So the honest framing of this piece is not “here are four animal-pharma stocks.” It is: here are two pure animal-health plays at opposite ends of the value chain (NGL at the molecule, Hester at immunity), one former pure-play that has just changed its spots into a human-plus-animal giant (Viyash), and one human-pharma exporter that the market sometimes files under animal health (Fredun). Understanding which is which is most of the work. Let’s take them in turn, climbing the value chain.

Part 5: NGL Fine Chem, The Molecule Specialist

BSE: 524774 | NSE: NGLFINE | Market cap: ~₹1,500 crore (late May 2026)

NGL Fine Chem is the cleanest pure-play in the basket and, not coincidentally, the one that just lived through the most instructive boom-bust-recovery cycle in the sector. If you want to understand why the API layer is a different animal (sorry) from the vaccine layer, read NGL’s last four years.

The business. Incorporated in 1981 and run by the Lawande and Nachane families (managing director Rahul Nachane), NGL manufactures veterinary APIs and intermediates: a portfolio of around 45 molecules across anti-parasitics, antibiotics, anti-inflammatories and the like, with animal-health API contributing roughly 95% of revenue. It exports across Europe, Asia Pacific, Latin America, the US, and a long tail of emerging markets. The top ten customers are about 29% of sales, and the top ten products are about 66%, so reasonable customer diversification sits on a more concentrated product base. This is a focused, founder-run, export-oriented veterinary API house. No human distraction, no biologics, just chemistry sold to formulators worldwide.

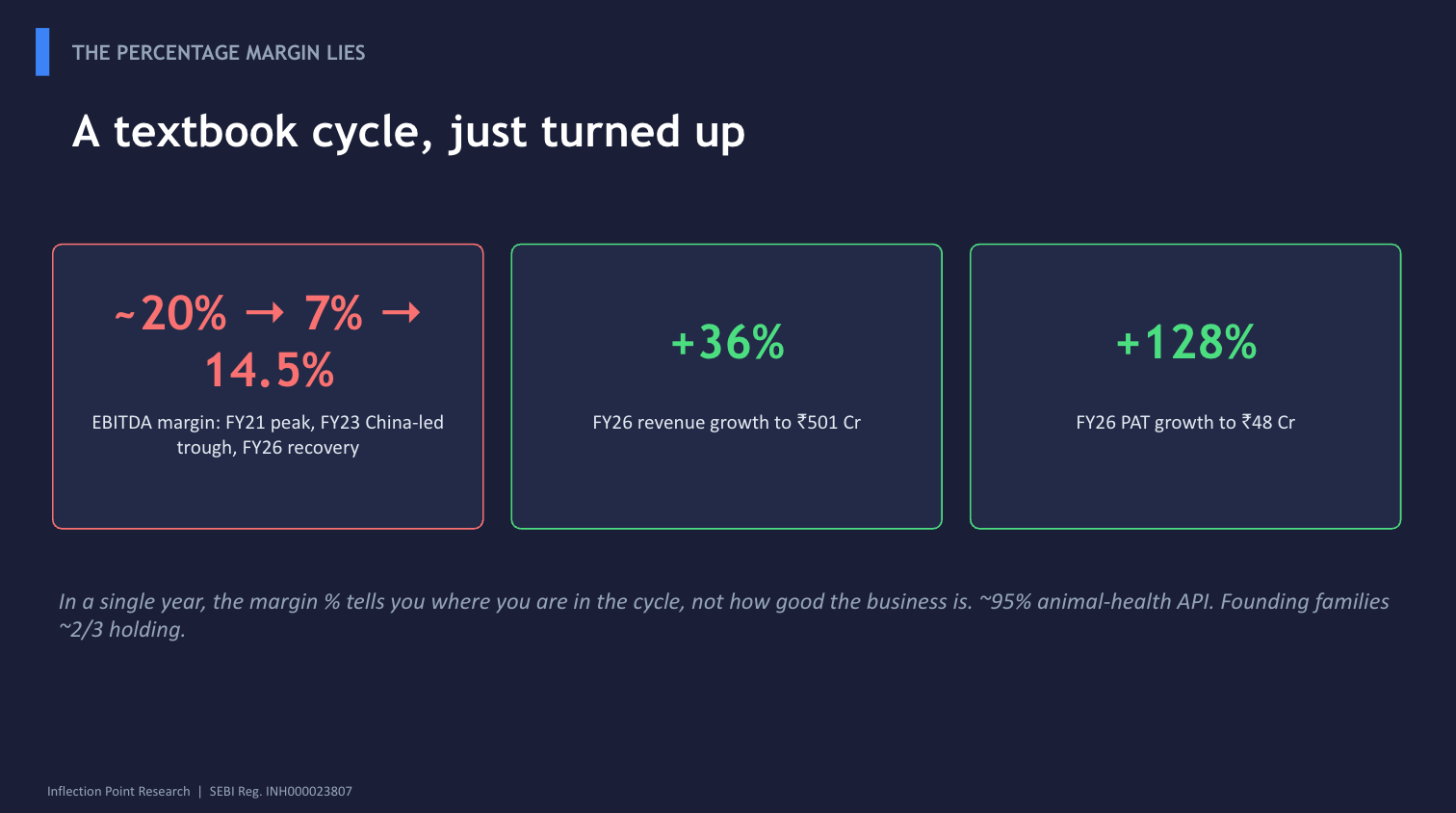

The financials, and why the percentage margin lies. Here is the cycle. NGL’s EBITDA margin ran above 20% in FY21, collapsed to around 7% in FY23 as Chinese oversupply and crashing realisations gutted the whole veterinary-API space, recovered partially in FY24, then fell back to 9.2% in FY25 as competition, weak realisations, and currency problems in markets like Africa and Pakistan bit again. FY25 revenue grew a modest 8.7% to ₹368 crore, but PAT nearly halved to ₹21 crore. On the screen, FY25 looked like a broken business.

It wasn’t broken; it was cyclical, and the cycle has turned hard. FY26 revenue jumped 36% to ₹501 crore, EBITDA more than doubled to ₹72.7 crore (a margin of 14.5%, up 531 basis points), and PAT grew 128% to ₹48 crore. The Q4 FY26 exit was even stronger: revenue up roughly 56% year-on-year, EBITDA margin back to 14.3%, PAT swinging from near-zero a year earlier to ₹13.5 crore. Management is now guiding for a steady-state EBITDA margin band of 15 to 18%, helped by partial cost pass-through to customers.

The lesson, which is the same lesson I keep hammering in commodity-linked businesses like KSH International, for an API maker, the percentage margin in any single year tells you where you are in the cycle, not how good the business is. The thing to track is whether realisations and volumes are recovering and whether the capacity coming online can be filled profitably.

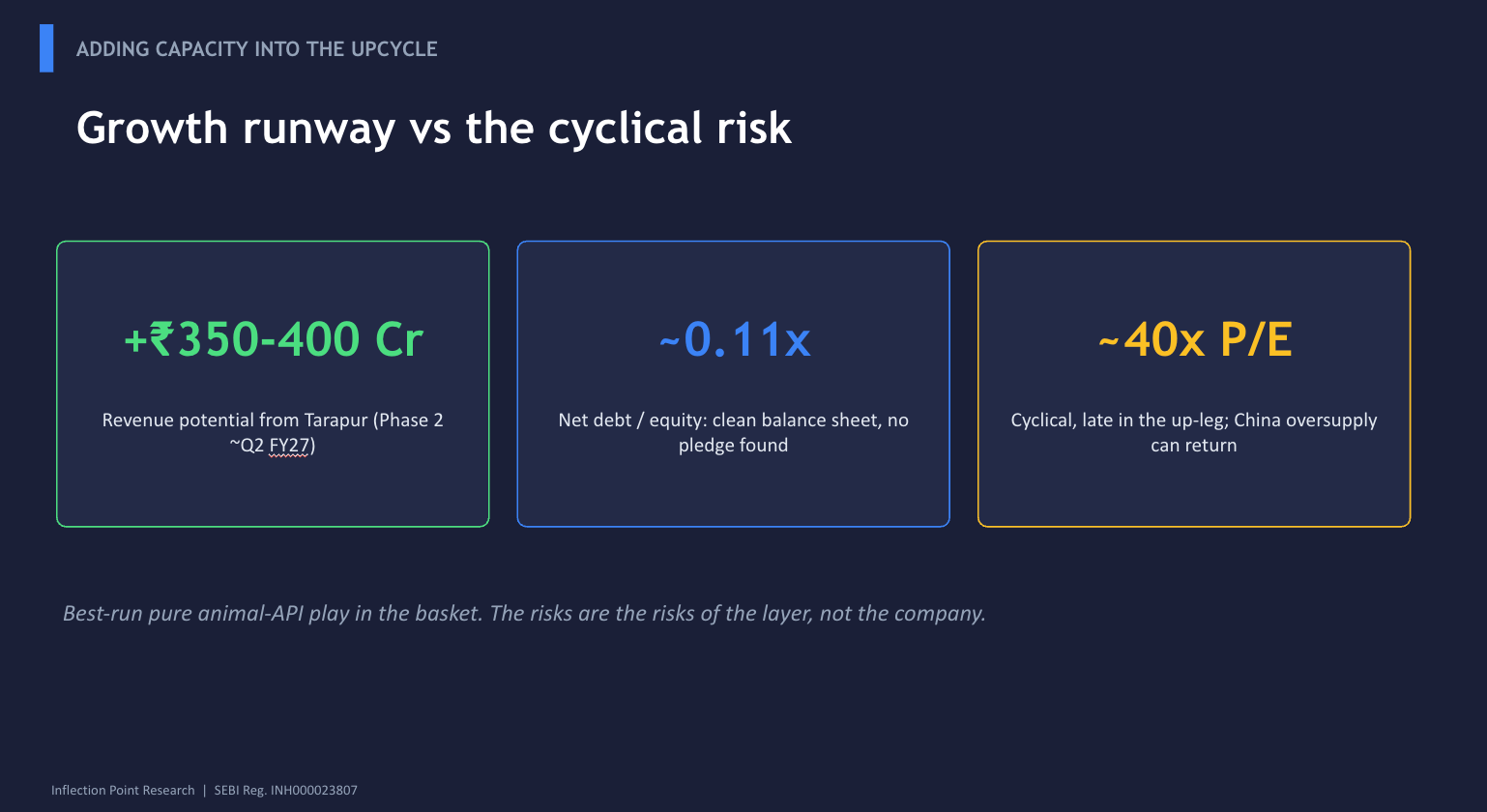

The growth engine. NGL has been investing through the downturn, which is the right time to do it. It has deployed about ₹183 crore of a planned ₹210 crore greenfield expansion at Tarapur. Phase 1 is already contributing; Phase 2 is expected to commercialise in early Q2 FY27, having slipped slightly on gas and labour availability. Management’s stated revenue potential from the new capacity is an incremental ₹350 to 400 crore, which, against a ₹501 crore FY26 base, is a near-doubling of the revenue runway if utilisation comes through. The company has also been pushing into Latin America and broadening the molecule count. This is a business adding capacity into a recovering cycle, which is the textbook setup for operating leverage if (and it is a real if) the cycle holds.

Balance sheet and governance. Conservative and clean. Net debt-to-equity is around 0.11, and debt-to-EBITDA is under 1x even after the capex, ROCE and ROE in the mid-teens. Promoter holding is high (the founding families collectively hold roughly two-thirds), I have seen no pledging, and the board carries genuine independent directors. There is no governance puzzle here that I can find, which is refreshing and rare in micro-cap land. The one thing to watch is simply the execution of the Tarapur ramp and the durability of the margin recovery.

The risks. They are the risks of the layer, not the company. Chinese oversupply can return and crush realisations again; the FY23 trough is a reminder that this is not a smooth compounder. Currency and geopolitical friction in Africa and Pakistan have hurt before. And at a P/E in the high-30s to low-40s on a recovering-but-still-cyclical earnings base, the market is already pricing in a good chunk of the upcycle. NGL is the best-run pure animal-API play I can find, but you are buying a cyclical at a point where the cycle has already turned up and the multiple knows it.

Part 6: Viyash Scientific, The Giant That Changed Shape

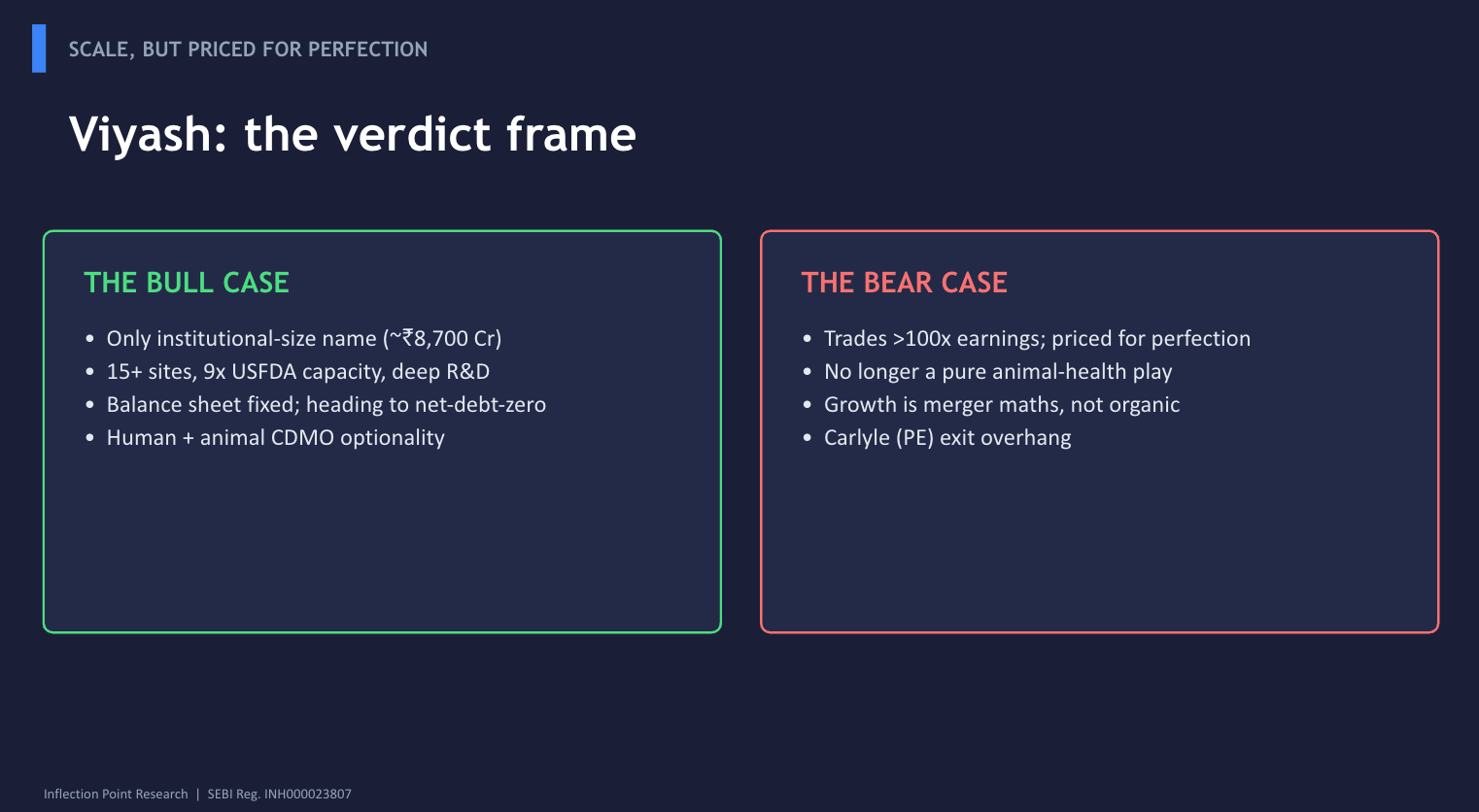

BSE: 512529 | NSE: SEQUENT | Market cap: ~₹8,700 crore (late May 2026)

This is the heavyweight of the group by a distance, roughly five to six times the market cap of the other three, and it is also the company whose identity has shifted most. Read this section less as “is it a good animal-pharma stock” and more as “what exactly am I buying now.”

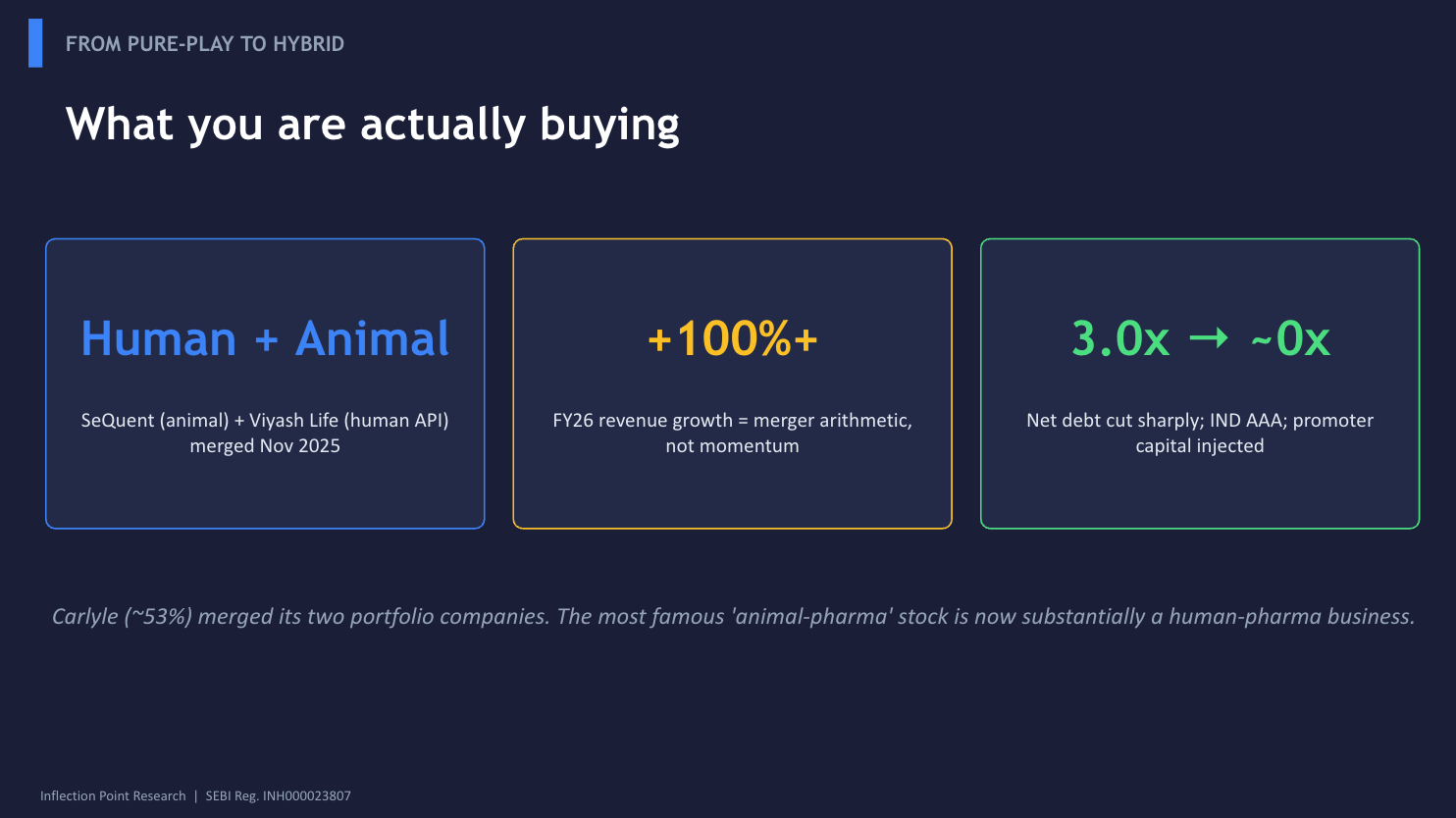

The history. SeQuent Scientific was, for years, India’s flagship pure-play animal-health company: APIs, finished formulations (under the Alivira brand) and analytical services for the veterinary market, with manufacturing across India, Spain, Brazil, Turkey and the US, and product registrations in over 90 countries. Private-equity firm Carlyle took control, holding about 53%. SeQuent was the name every animal-health discussion in India started with.

The merger. In September 2024, Carlyle announced it would merge its other, privately held portfolio company, Viyash Life Sciences (a human-API and intermediates platform founded in 2019 by Hari Babu Bodepudi, the former global COO of Mylan), into listed SeQuent. The roughly ₹8,000 crore all-stock combination cleared shareholders with 99.98% approval, became effective in November 2025, and the merged group was renamed Viyash Scientific in January 2026. Bodepudi became group CEO and, with a personal capital infusion of around ₹400 crore, the second-largest shareholder behind Carlyle.

The strategic logic is sound. The combined entity has 15 to 16 manufacturing sites, a roughly nine-fold expansion in USFDA-approved capacity, a far deeper R&D bench, and access to 150-plus countries across both human and animal health. Crucially, the merger fixed SeQuent’s balance sheet: net debt to operating profit improved from about 3.0x in March 2025 to around 0.9x by December 2025, and with Bodepudi’s infusion, the group is heading toward roughly net-debt-zero. ICRA rates it IND AAA. The combined business targets around ₹650 crore of annual operating profit and a CDMO build-out serving global innovators.

What you are actually buying. A human-plus-animal integrated pharma platform, not a pure animal-health play. The first combined-entity results (the December 2025 quarter was the first reported on a merged basis) point to a merged FY26 revenue in the region of ₹3,400 to 3,500 crore, up well over 100% year-on-year, but that growth is overwhelmingly the merger arithmetic of bolting on Viyash’s human business, not organic animal-health growth. (These merged full-year figures are early and partly aggregator-sourced; verify against the audited FY26 results and the company’s own investor presentation before you rely on them.) It is the same headline-growth illusion I flagged on Quality Power’s Mehru consolidation in the power piece: a 100%-plus revenue number that is structure, not momentum.

Valuation and governance. This is the expensive end of the basket. The stock trades on a trailing P/E north of 100x and a price-to-book near 10x, with reported ROE still in low single digits because the merged earnings base is depressed by one-off merger and ESOP costs. The bull case is that as synergies land, leverage falls, the CDMO ramps and margins normalise, the earnings catch up to the valuation. The bear case is that you are paying a venture-like multiple for an integration that still has to be executed, in a business that is now half human-pharma generics, one of the most competitive arenas on earth.

On governance, the framing is different from the family-run names. This is a private-equity-controlled company with professional management. That brings discipline and a clean balance-sheet philosophy, but it also brings the eternal PE question: Carlyle is a financial owner with an eventual exit, and how and when it monetises its majority stake is a structural overhang you should price in. The integration-synergy delivery and the path of Carlyle’s holding are the two things I would watch above all else.

Viyash is the scale player, the global platform, and the highest-quality manufacturing footprint of the four. It is also no longer the pure animal-health champion its old name conjures, and it is priced for a great deal to go right.

Part 7: Fredun Pharmaceuticals, The Exporter Wearing a Vet Coat

BSE: 539730 | Market cap: ~₹1,300 crore (late May 2026)

Fredun has been one of the great micro-cap stock-price stories of the past year, up well over 100% (by some measures over 200%) and recently announcing a 2:1 bonus. It is also the company in this piece whose connection to the animal-health theme is the loosest and whose governance flags are the most numerous. Both things are true at once, and I refuse to airbrush either.

The business. Promoted by the Medhora family, Fredun is a Mumbai-based formulations manufacturer: tablets, syrups, capsules, ointments across antihypertensives, antidiabetics, antiretrovirals, narcotics, plus nutraceuticals, cosmeceuticals, diagnostics and an animal-healthcare line. It is heavily export-led, shipping to Africa, Southeast Asia, the CIS region and Latin America. The headline is “holistic healthcare provider,” which is another way of saying diversified across a lot of small things, of which animal health is one. Animal-health activity is partly run through group entities (Fredun Healthcare, Fredna Enterprises) rather than entirely inside the listed company, so the precise animal-health revenue share inside the listco is not cleanly disclosed and is, in any case, modest. (If you want to size the animal-health exposure exactly, dig the segmental and related-party disclosures out of the annual report; the public sources do not break it out cleanly.)

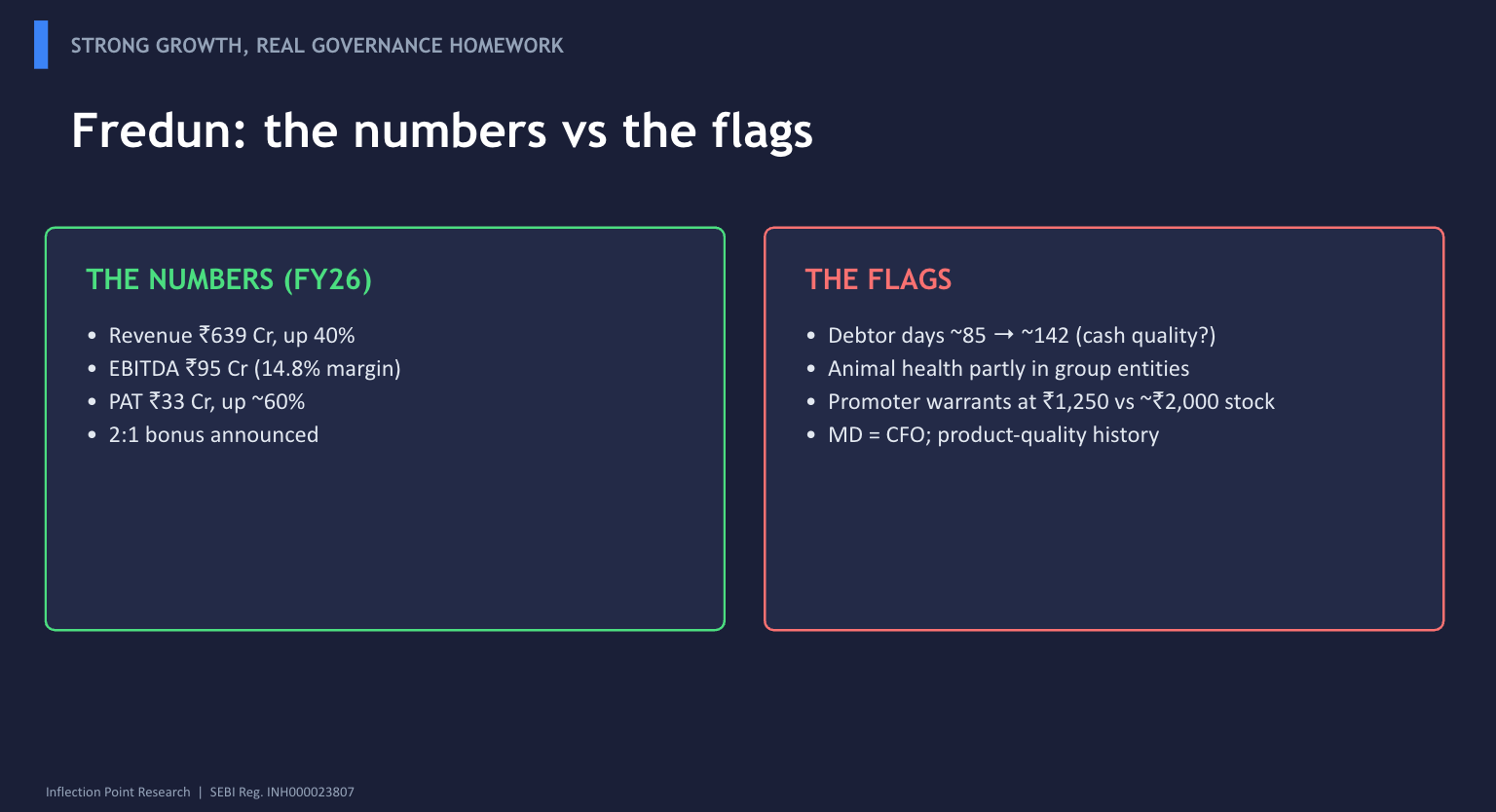

The financials. Genuinely strong, on the numbers as reported. FY26 revenue grew about 40% to ₹639 crore, EBITDA jumped 72% to ₹95 crore (a margin of 14.8%, expanding nicely), and PAT rose around 60% to ₹33 crore, with profit growing faster than revenue, a good sign of operating leverage. FY25 was ₹456 crore revenue, ₹55 crore EBITDA, ₹21 crore PAT, so this is a business that has roughly doubled revenue in two years. A new 40,000-square-foot facility in Palghar (its fifth unit), expected to be operational by October 2026, is slated to support veterinary products, nutraceuticals and formulations. On growth alone, Fredun is firing.

Now, the governance section, which is where I earn my registration. There are several flags here, and I would not publish a piece that buried them.

First, working capital. Debtor days have reportedly stretched from around 85 to roughly 142. For an export-led formulations business, a near-doubling of receivable days is a real cash-flow-quality question: is the growth being bought with ever-looser credit terms? This is the single number I would interrogate hardest. Strong reported profit alongside ballooning debtors is the classic pattern that warrants a careful look at cash conversion.

Second, the structure. Housing part of the animal-health business in group entities rather than the listco creates related-party complexity and makes the consolidated picture harder to read. It is not damning in itself, but it is the kind of structure that requires you to read the related-party notes properly.

Third, the promoter warrants. Promoters have been converting warrants issued to themselves at ₹1,250 a share while the stock subsequently traded up toward ₹2,000. Issuing cheap warrants to insiders ahead of a run is legal and common, and it does inject promoter capital, but it also means insiders captured a chunk of the upside on preferential terms. Promoter holding sits around the high-40s percent and has been rising via these conversions, though it had drifted down over the prior three years.

Fourth, history. Fredun has had product-quality and regulatory blemishes in its past, and the managing director also holds the CFO role, a concentration of financial authority that good governance practice generally discourages. The credit rating is a modest IVR BBB, which tells you this is not a fortress balance sheet.

The honest read. Fredun is a fast-growing, export-led human-formulations company that is being partly narrated as an animal-health play it is mostly not, trading on a P/E in the high-20s to high-30s, depending on the day, with a cluster of governance and working-capital items that a careful investor must price in rather than wave away. The momentum is real. So are the flags. If you are buying Fredun, buy it understanding it is a diversified pharma exporter with a vet side-line and a watch-list of governance items, not a clean animal-health bet.

Part 8: Hester Biosciences, The Immunity Fortress

BSE: 524669 | NSE: HESTERBIO | Market cap: ~₹1,500 crore (late May 2026)

We finish at the top of the value chain, with the only biologics company in the group and, in business-quality terms, the purest and most defensible animal-health franchise of the four.

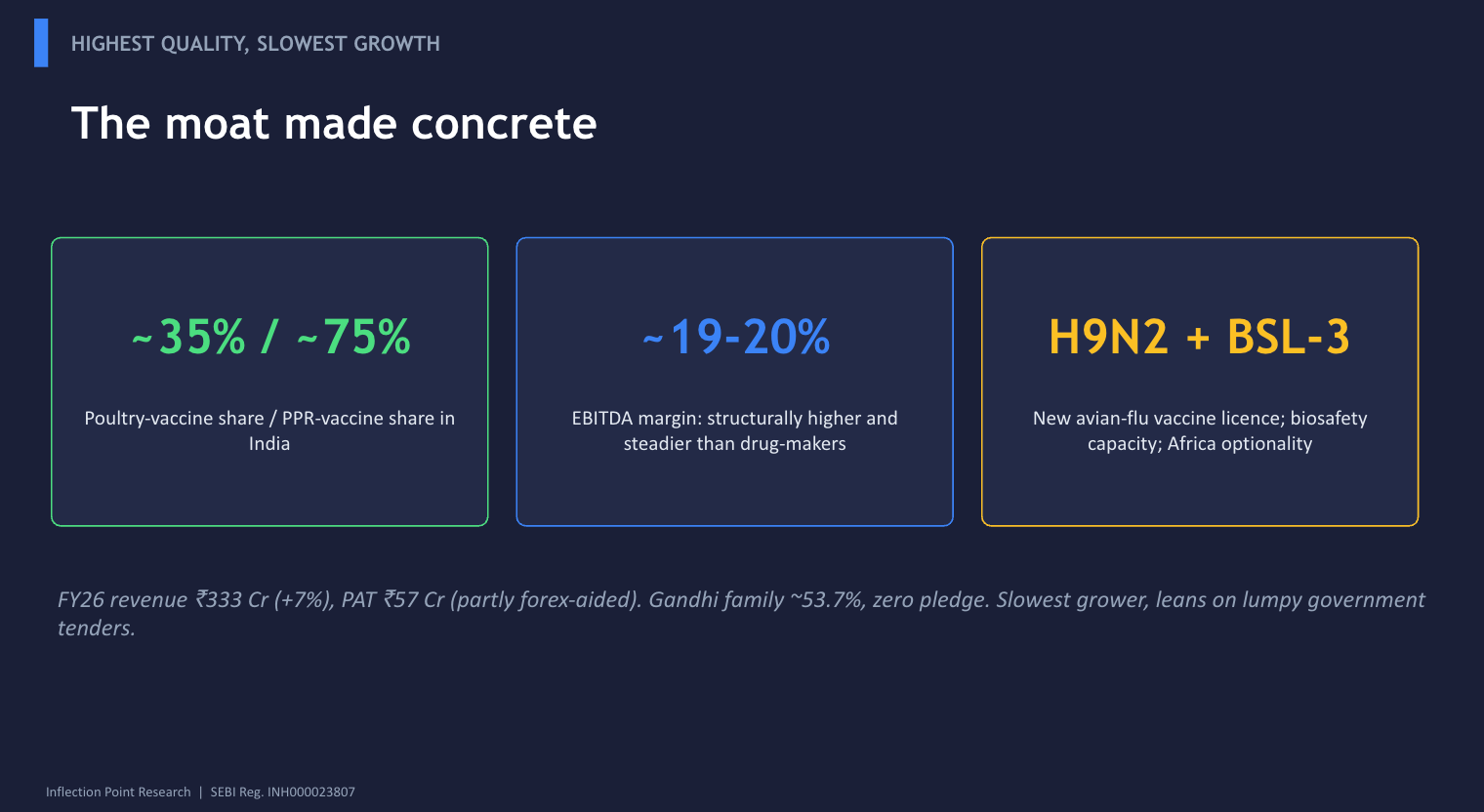

The business. Founded in 1987 by Rajiv Gandhi (still the CEO and MD, with daughter Priya Gandhi as executive director), Ahmedabad-based Hester is India’s second-largest poultry-vaccine manufacturer, with roughly 35% share of the poultry-vaccine market and around 75% share in PPR (peste des petits ruminants, “goat plague”) vaccines. It operates what it describes as Asia’s largest single-location animal-biological facility, across four verticals: poultry vaccines, poultry health products, animal vaccines and animal health products, plus diagnostic and seroprofiling services. Its vaccine platforms span chick-embryo, continuous cell line, tissue culture and fermentation-based live and inactivated vaccines. It has manufacturing and operations in India, Nepal and Tanzania, and partnerships with the Gates Foundation and GALVmed for livestock vaccines in Africa.

This is the moat layer made concrete. You cannot replicate a biosafety-contained, multi-platform, regulator-licensed vaccine business by buying a reactor. The barriers are biological, regulatory and reputational, and they are why Hester structurally earns higher and steadier EBITDA margins (around 19 to 20%) than the mid-teens of the API and formulation players.

The financials. FY26 consolidated revenue grew about 7% to ₹333 crore, and PAT nearly doubled to ₹57 crore from ₹29 crore. The board declared a healthy ₹11-per-share dividend, and net debt is modest at around ₹70 crore. So far, so good. But two pieces of nuance matter.

First, the quality of the FY26 profit jump. A meaningful part of the near-doubling in PAT was helped by forex gains, not purely operating performance, and Q3 FY26 actually saw profit fall year-on-year despite revenue growth. The underlying EBITDA trajectory is solid but less explosive than the headline PAT number suggests, so do not extrapolate “profit doubled” as a run-rate.

Second, the divisional split. Hester’s poultry business has been the strong engine while the animal-health (ruminant and companion) division has been weak, dragged by delays in the government programme offtake. (The exact magnitude of the animal-division decline varies across sources; confirm the FY26 segmental numbers from Hester’s own results presentation before quoting them.) Government tenders are a double-edged sword here: a structural growth vector when they flow, a source of lumpiness and disappointment when they stall.

The catalysts. Two are concrete. Hester has received a manufacturing licence for an inactivated H9N2 avian-influenza vaccine, developed with ICAR-NIHSAD technology, which lands directly into the biosecurity priority I flagged earlier and opens both domestic and export opportunities. And it has capitalised a BSL-3 (biosafety-level-3) facility and is expanding capacity at its Gujarat site, which raises the ceiling on what it can manufacture. The Africa operations (Tanzania, plus the Gates and GALVmed livestock-vaccine partnerships) are the long-dated optionality. There is also a neat intra-sector footnote: Hester acquired Alivira’s India animal-health business (Alivira being SeQuent’s, now Viyash’s, brand) for ₹26.5 crore back in 2023, a small reminder of how interconnected these four names actually are.

Balance sheet and governance. Clean. Promoter (the Gandhi family) holds around 53.7%, has filed a zero-encumbrance declaration for FY26, and the CEO’s reappointment passed with 99.54% shareholder approval. Modest debt, real dividends, founder still at the helm after nearly four decades. The governance picture is among the most straightforward of the four.

The risks. The flip side of the moat is that Hester is a slow-growth compounder: its five-year revenue growth has been in the low double digits at best, and the stock has de-rated, trading well below its 52-week high. Government-programme dependence makes quarters lumpy. And while the vaccine moat is durable, it does not translate into rapid top-line growth the way the API upcycle is currently flattering NGL or the merger arithmetic is flattering Viyash. You are buying the highest-quality, highest-moat, most-defensible business in the group, but also the slowest grower, at a more reasonable mid-20s P/E.

Part 9: Four Rungs, Four Risk Profiles

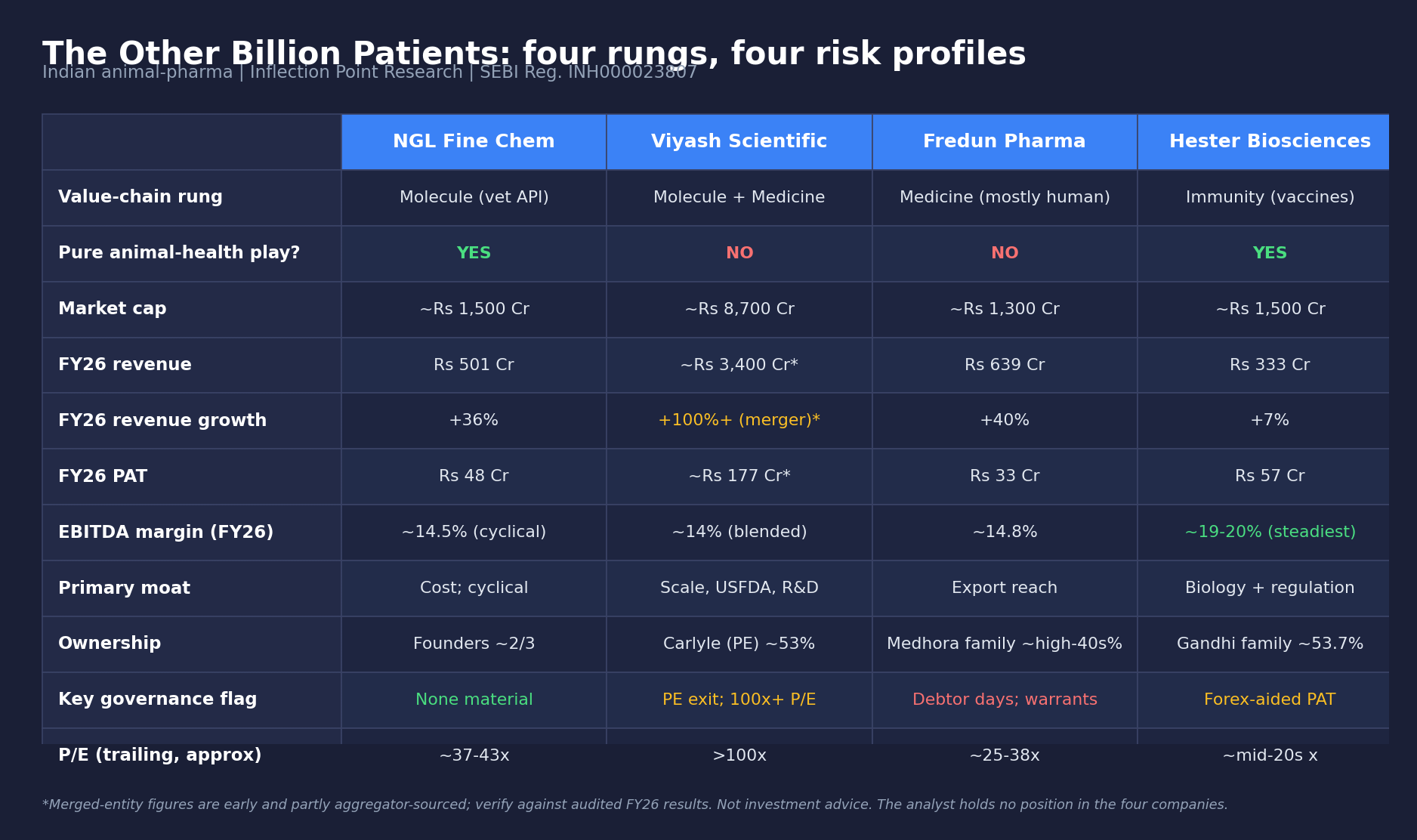

These are not four versions of the same bet. They are four different exposures to one theme, on different rungs of the value chain, with genuinely different risk profiles. The comparison table below is the one to screenshot; the numbers are compiled from company results, exchange filings and data aggregators, and the flagged figures should be verified against primary sources before you act on them.

The portfolio logic falls out of the table. NGL is the cyclical operating-leverage bet: cheapest exposure to the API upcycle, highest beta to realisations, best balance sheet of the small caps, but you are late to a cycle the market has already spotted. Viyash is the scale-and-platform bet: the only institutional-size name, the cleanest global footprint, but priced for perfection and no longer the pure animal play its history implies. Fredun is the momentum-and-execution bet: fastest revenue growth, most governance homework required, loosest tie to the actual theme. Hester is the quality-and-moat bet: the most durable franchise and the only true vaccine play, but the slowest grower and the most exposed to government-tender timing.

Part 10: How To Actually Think About This Theme

Let me compress the whole argument into something usable.

First, the structural opportunity is real and under-penetrated. The world’s largest animal population, about 3% of global animal-health spend, a commercialising protein economy, a government that has become a structural buyer of vaccines and generics, and a companion-animal wave on top. This is a genuine multi-decade catch-up story, not a narrative.

Second, value capture rises as you climb the chain. Molecule is cyclical and China-exposed. Medicine is competitive and working-capital-heavy. Immunity is the fortress. If you are paying for “animal-pharma exposure,” be precise about which rung you are buying, because their economics are not remotely the same.

Third, read the label before the ticker. Only NGL and Hester are pure animal-health businesses. Viyash is now a human-plus-animal platform whose triple-digit revenue growth is merger arithmetic. Fredun is a human-formulations exporter with a vet side-arm. The “four animal-pharma stocks” framing is the mistake; the two-pure-and-two-adjacent framing is the reality.

Fourth, the cleanest businesses and the cheapest stories are not the same names. Hester has the best business quality and governance but the slowest growth. NGL has the cleanest pure-play exposure and a fine balance sheet but is a cyclical late in an up-leg. Viyash has the scale,\ but the richest valuation and a PE-exit overhang. Fredun has the fastest growth but the longest governance checklist. There is no single “obvious” pick, which is exactly why a sector lens beats a single-stock punt here.

Fifth, sizing beats picking. Three of these four are sub-₹1,500-crore micro/small caps with the attendant liquidity and volatility risk, and several have already re-rated hard over the past year, compressing the margin of safety. Whatever you conclude, this is a basket to approach with position sizes that respect the cyclicality (NGL), the valuation (Viyash), the governance flags (Fredun) and the slow-growth reality (Hester), rather than a single high-conviction bet at these prices.

Sixth, the four things actually worth watching over the next few quarters are not headline revenue. They are: margin durability and the Tarapur ramp at NGL (does the API upcycle hold and does the new capacity fill profitably); synergy delivery, deleveraging and Carlyle’s stake at Viyash; debtor days and cash conversion at Fredun; and the poultry-versus-animal-division mix plus the H9N2 and government-tender flow at Hester. If those move the right way, the structural thesis holds even when the quarterly prints get noisy.

Part 11: What I’m Watching

For NGL Fine Chem: Whether the FY26 margin recovery (14.5% EBITDA, guidance of 15 to 18%) holds or fades as Chinese realisations move. The Tarapur Phase 2 commissioning is expected in early Q2 FY27 and the pace of utilisation against the ₹350 to 400 crore incremental revenue potential. Any sign of a fresh China-led price war in core molecules.

For Viyash Scientific: The first clean full-year of merged results to separate genuine organic growth from merger arithmetic. The trajectory of net debt toward zero and the realisation of the targeted synergies. The CDMO ramp. And, structurally, any signal on how and when Carlyle intends to monetise its majority stake.

For Fredun Pharmaceuticals: Debtor days, debtor days, debtor days. Whether cash flow from operations keeps pace with the reported profit growth. The Palghar facility ramp from October 2026. The actual disclosed animal-health revenue share, and any further promoter warrant or related-party activity.

For Hester Biosciences: The recovery (or not) of the animal-health division against the strong poultry base. The commercial ramp of the H9N2 avian-influenza vaccine and the contribution from the new BSL-3 capacity. Government-tender flow for PPR, FMD and brucellosis under the national programme. The Africa (Tanzania, Gates/GALVmed) optionality turning into real revenue.

For the sector overall: The pace of government animal-health spending in the FY27 Budget and the rollout of Pashu Aushadhi. Avian influenza outbreak news, which pulls vaccine demand forward. The regulatory direction on veterinary antibiotics, which reshapes the molecule mix. And the companion-animal data: every Mars-style entry and every step toward pet insurance is a pull-through at the highest-margin end of the chain.

Part 12: A Closing Thought

There is something fitting about ending a run of pieces on electrons and glass with one on animals. The power grid and the fibre network are the infrastructure of the machine economy. Livestock and poultry and the family dog are the infrastructure of the protein-and-companionship economy, the older, more fundamental one, the one that fed us long before it powered us.

India has spent decades building the world’s largest animal population and almost no time learning to keep it medicated, vaccinated and productive at the rate richer countries take for granted. That gap is closing now, slowly, unevenly, with government money and commercial density and a billion small economic decisions by farmers and pet owners pushing it shut. The companies that learned to make the molecules, formulate the medicines and grow the vaccines for that population are sitting in front of a long, unglamorous, compounding tailwind.

The trick, as always, is to know which layer of the chain you are buying, and to read the label before you read the ticker. Two of these four are what they say they are. Two are not. The market will eventually price the difference. Your job is to see it first.

See you at the next inflection point.

Karnik

Inflection Point Research

GET TWO FREE IPR SAMPLE REPORTS

“The Other Billion Patients” is exactly the kind of structural, under-penetrated opportunity that Inflection Point Research narrows into specific, actionable company names for subscribers. Two free sample reports show that full framework applied to individual stocks: Gravita India (Future Titans tier, lead recycling with a regulatory tailwind, BUY framework) and Kalyani Cast Tech (Microcap Mavericks tier, container manufacturer with a founder moat, watchful-hold framework).

Get your two free samples here: https://www.inflectionpointresearch.in/free-sample-research-reports

No payment required. SEBI Reg. INH000023807.

Portfolio Disclosure

I do not currently hold positions in NGL Fine Chem (NGLFINE), Viyash Scientific (SEQUENT), Fredun Pharmaceuticals (FREDUN) or Hester Biosciences (HESTERBIO). I have no position in any other company specifically referenced in this piece. I may initiate, add to, reduce or exit any position at any time based on changes in fundamentals or portfolio rules. This disclosure is as of the date of publication.

SEBI Disclosure

This report is published by Inflection Point Research, a SEBI-registered Research Analyst (Registration No. INH000023807). This content is for informational and educational purposes only and should not be construed as investment advice, an offer to buy or sell securities, or a recommendation of any specific investment action. Readers should conduct their own due diligence and consult their financial advisers before making investment decisions. Past performance is not indicative of future results. Equity investments are subject to market risks. All financial data requires independent verification from primary sources before use in investment decisions.

If this piece was useful to you

Forward it to one person who follows the human-pharma names but has never thought about the animal half of the chain. That is how this newsletter finds the right readers, one thoughtful forward at a time.

Until next week,

Karnik

You’re awesome sir

What a compilation

Very very useful sir

🤝🤝