The 10-Bagger Problem: Why Finding Them Is the Easy Part

A framework for identifying compounding machines, and the harder, lonelier discipline of not destroying the returns you have already earned

There is a specific kind of investor pain that nobody talks about enough.

Not the pain of losing money. That one gets discussed constantly. Books are written about it. Risk management frameworks exist precisely to address it. Every brokerage has a “stop-loss” feature. Nobody has a “hold-your-winner” feature.

The pain I am talking about is quieter, and in some ways, more financially damaging. It is the pain of having been right: spectacularly, embarrassingly right, and still walking away with a fraction of what you should have made.

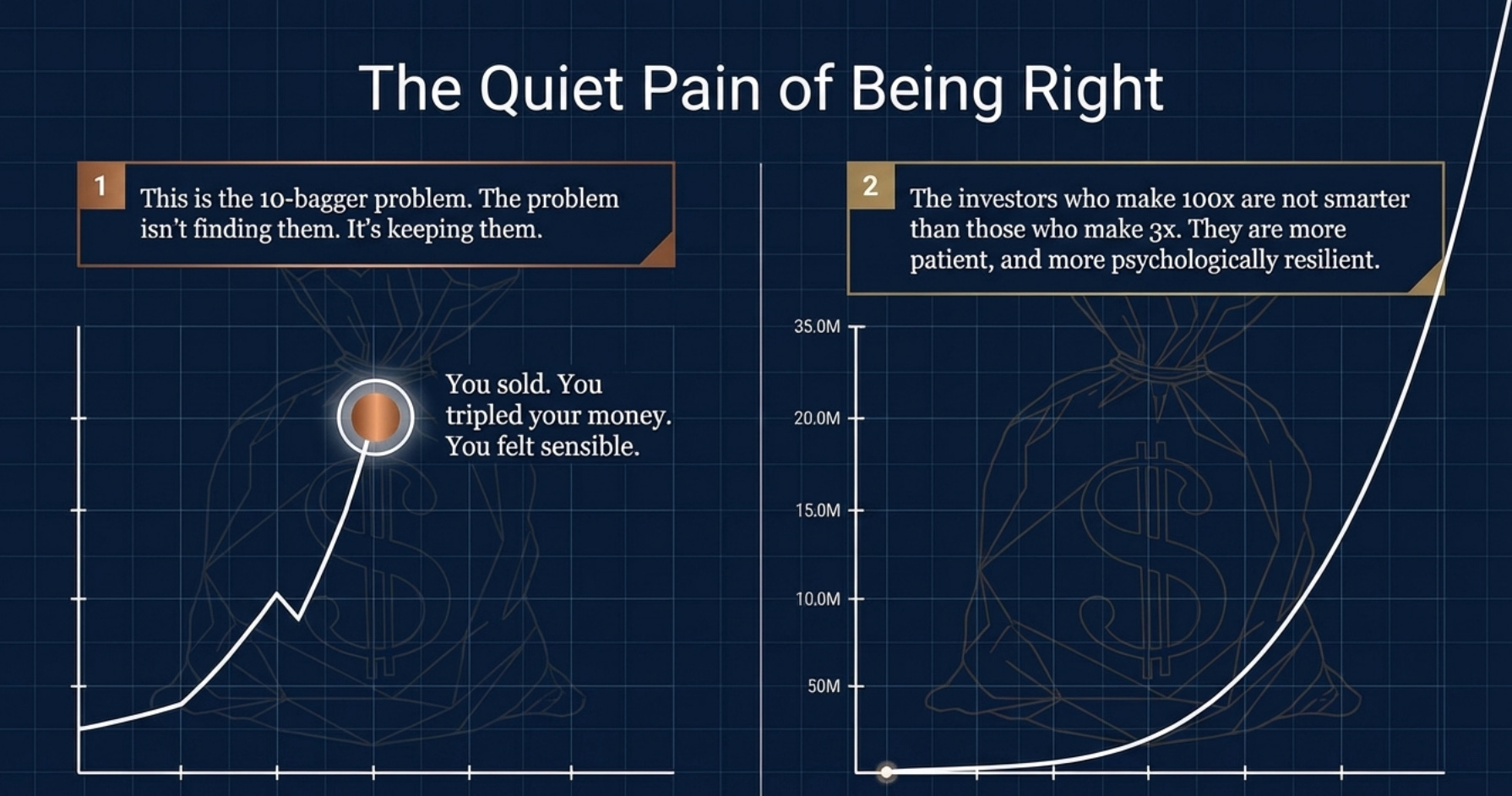

You found the stock at ₹200. You watched it go to ₹600. You thought: I have tripled my money, time to be sensible. You reinvested in something “cheaper.” The original stock went to ₹4,000. You watched that number, alone, in silence, for years.

This is the 10-bagger problem. And the problem is not finding them. It is keeping them.

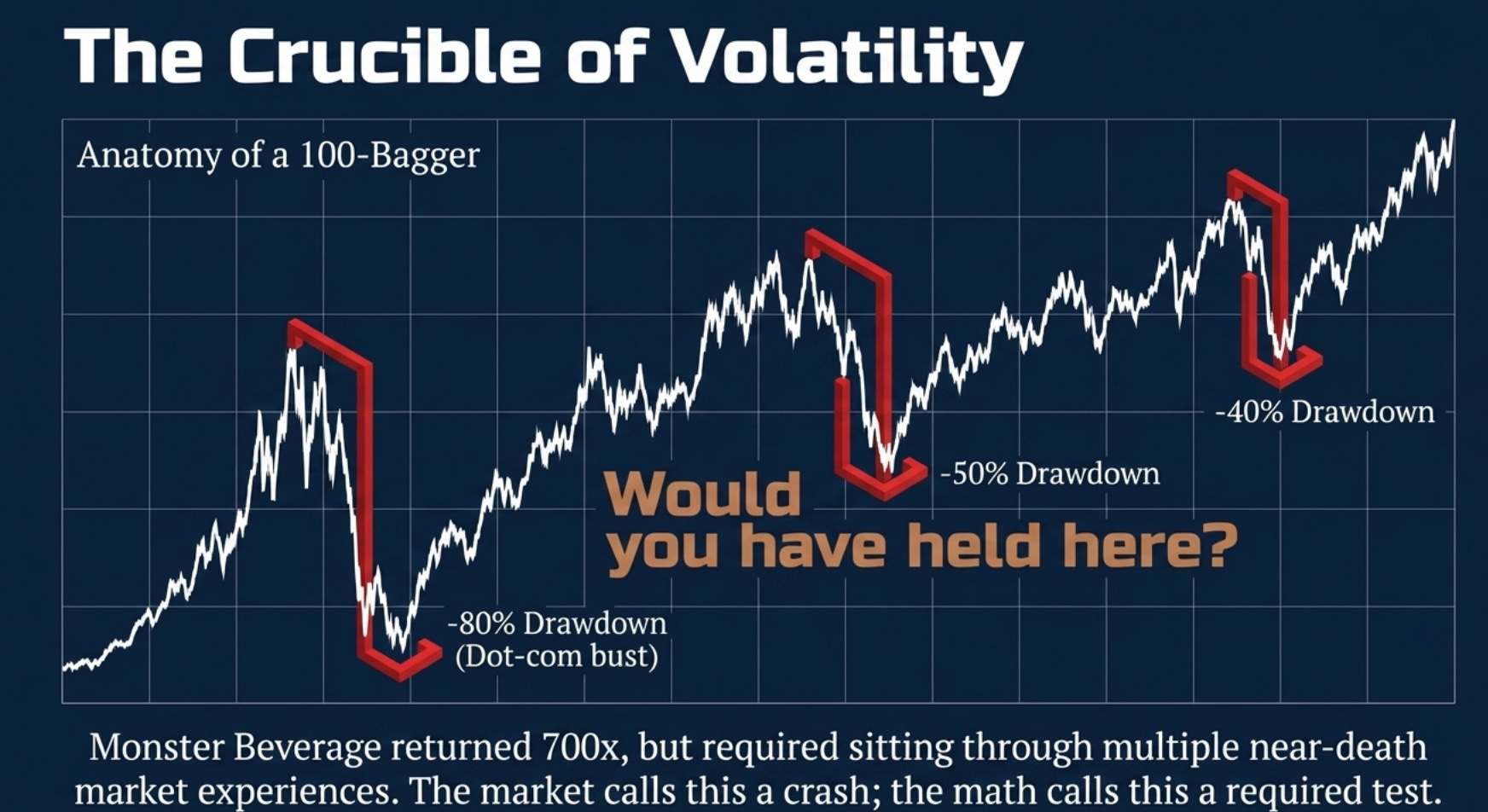

Christopher Mayer spent years studying stocks that returned 100 times or more, so-called “100 baggers,” and the single most striking finding was not about balance sheets or growth rates. It was behavioural. He found that most of these stocks spent significant periods looking terrifyingly expensive by conventional metrics. They corrected 30%, 50%, even 70% along the journey. They tested the conviction of their holders at every stage. The investors who made 100x were not necessarily smarter than those who made 3x. They were more patient and more psychologically resilient.

This piece is about both sides of the problem: the analytical framework for identifying companies with genuine multi-bagger potential, and the far harder, far less glamorous work of doing nothing once you have found them.

The Twin Engines: What a 10-Bagger Actually Is

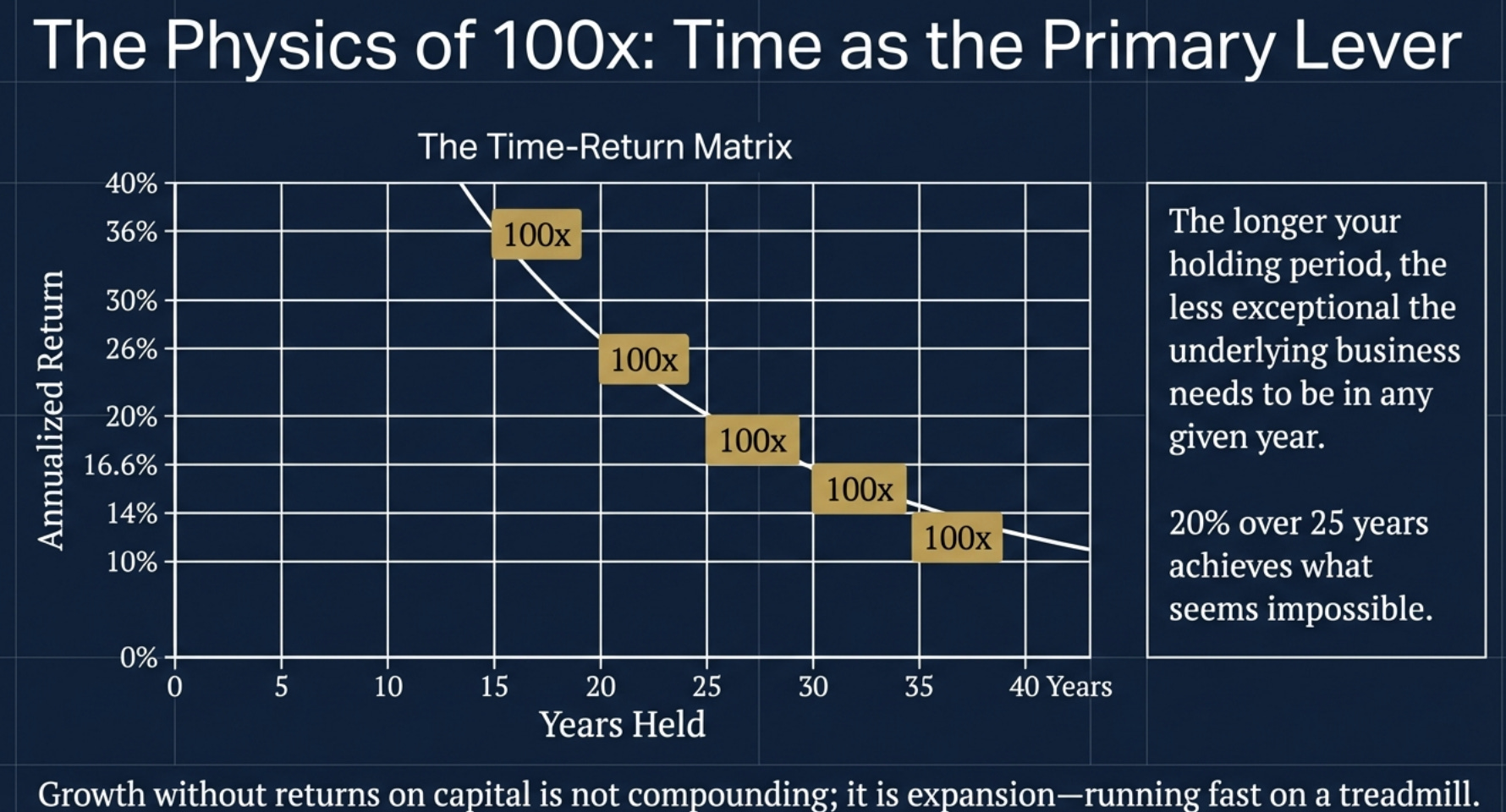

Before anything else, you need to understand what a 10x return looks like in mathematical terms. Because once you internalise the maths, the screening process becomes almost obvious.

A 10x return over ten years requires a 26% annualised return. Over fifteen years, just 17% per annum. Over twenty years, a mere 12.5%. Time is doing extraordinary amounts of work here, and that is the first and most underappreciated insight: the longer your holding period, the less exceptional the underlying business needs to be in any given year.

But here is where most frameworks go wrong. They focus on growth rates in isolation. Revenue growing at 25% a year. Profits compounding at 30%. These numbers are seductive, but they are incomplete. Growth without returns on capital is not compounding; it is expansion. The business equivalent of running very fast on a treadmill. You are moving, but you are not going anywhere wealth-building.

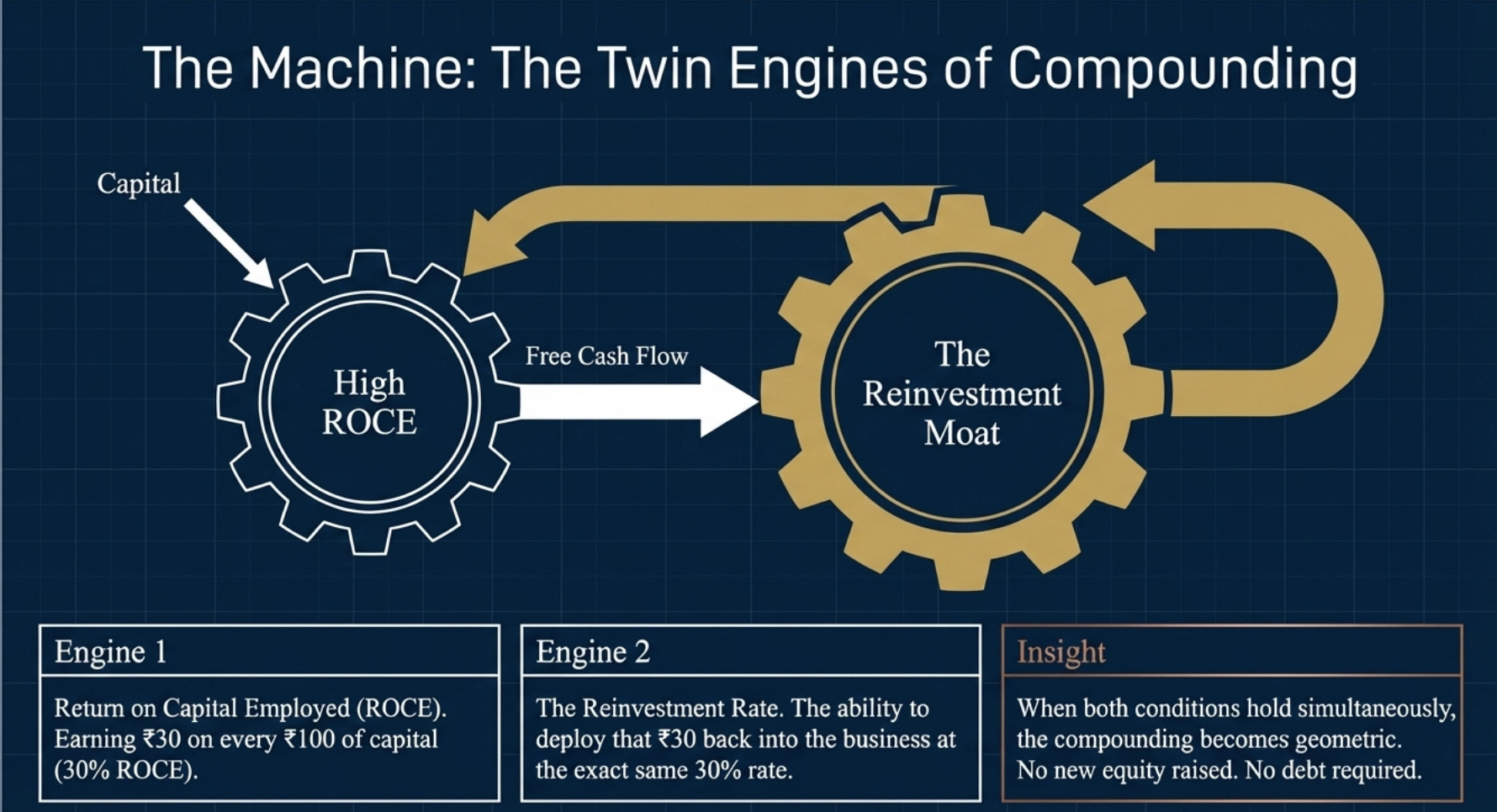

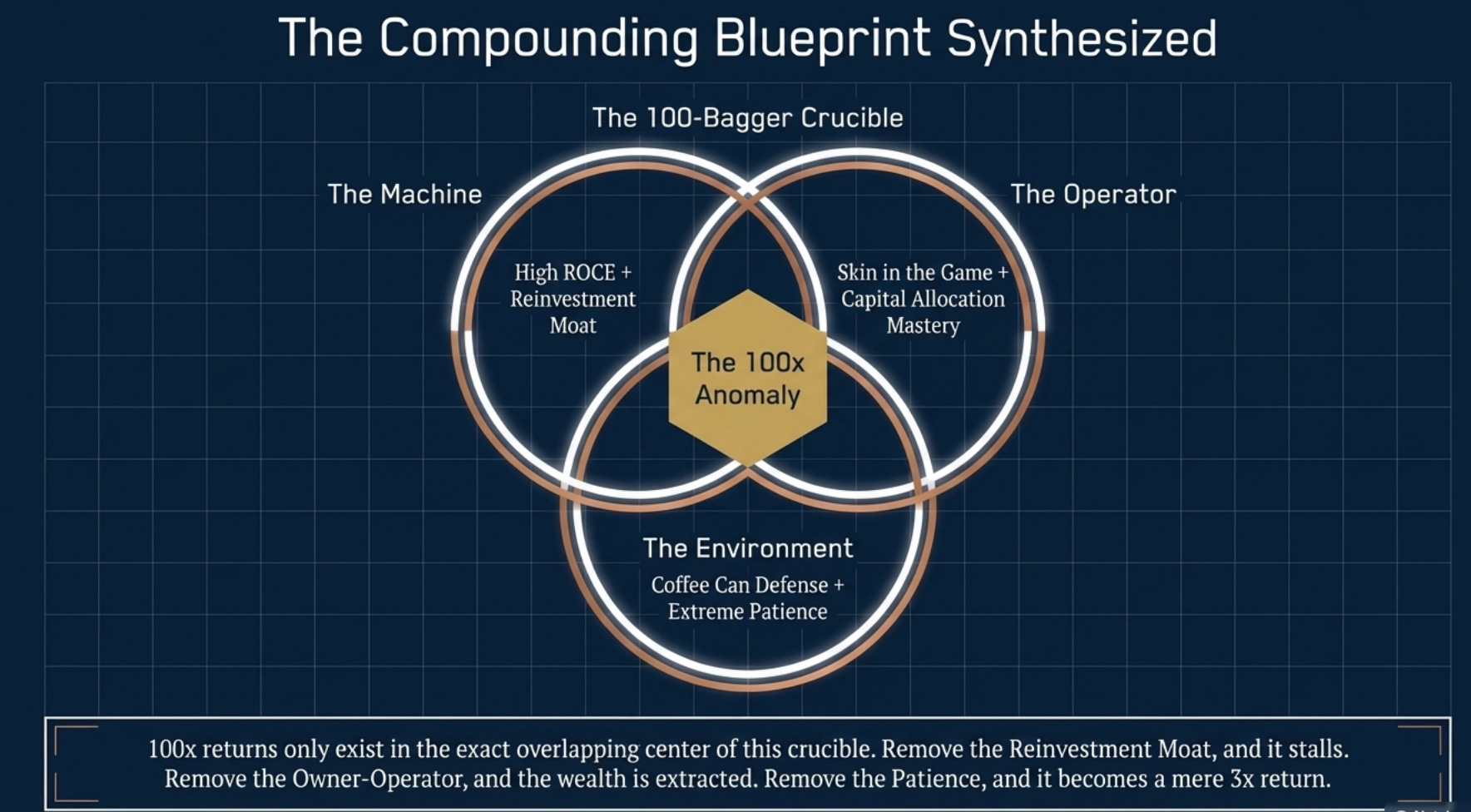

The real engine of multi-bagger returns is a specific combination: high returns on incremental capital, combined with the ability to reinvest large portions of earnings at those high rates, over a sustained period.

Buffett has articulated versions of this for fifty years, but the clearest formulation is simple: the truly exceptional businesses are not just those that earn high returns, but those that can redeploy the capital they generate at similarly high rates. When both conditions hold simultaneously, the compounding becomes geometric and the results, over a decade, become jarring.

Let me make this concrete. Imagine a business earning a 30% return on capital employed (ROCE). In year one, it earns ₹30 on every ₹100 of capital. If it retains and reinvests that ₹30 at the same 30% rate, in year two it earns ₹39 on ₹130 of capital. By year ten, that original ₹100 has compounded to approximately ₹1,378. No new equity raised. No debt required. Just reinvestment at a high rate, compounding quietly.

This is the twin-engine framework. The first engine is the ROCE itself: the return the business earns on what it deploys. The second, and deeply underappreciated engine, is the reinvestment rate, meaning what fraction of free cash flow the business can put back into new growth at the same or similar returns.

Most businesses have one engine running. A mature consumer staples company might earn 40% ROCE but have nowhere productive to reinvest; the market is saturated, growth is single-digit, so cash accumulates or gets returned as dividends. A high-growth startup might be expanding rapidly but earning deeply negative returns on capital, growing fast but destroying value with every rupee spent. Neither is a genuine compounder.

The 10-bagger candidates are those rare businesses where both engines run simultaneously: high returns on capital today, combined with a long enough runway to keep reinvesting at those rates. In investment literature, this is sometimes called a “reinvestment moat,” and finding it is the starting point for everything else.

What These Businesses Look Like in the Wild

So what do genuine multi-bagger candidates actually look like? Across the study of extraordinary returners in both global and Indian markets, a set of qualitative traits appears with remarkable consistency.

The Owner-Operator at the Helm

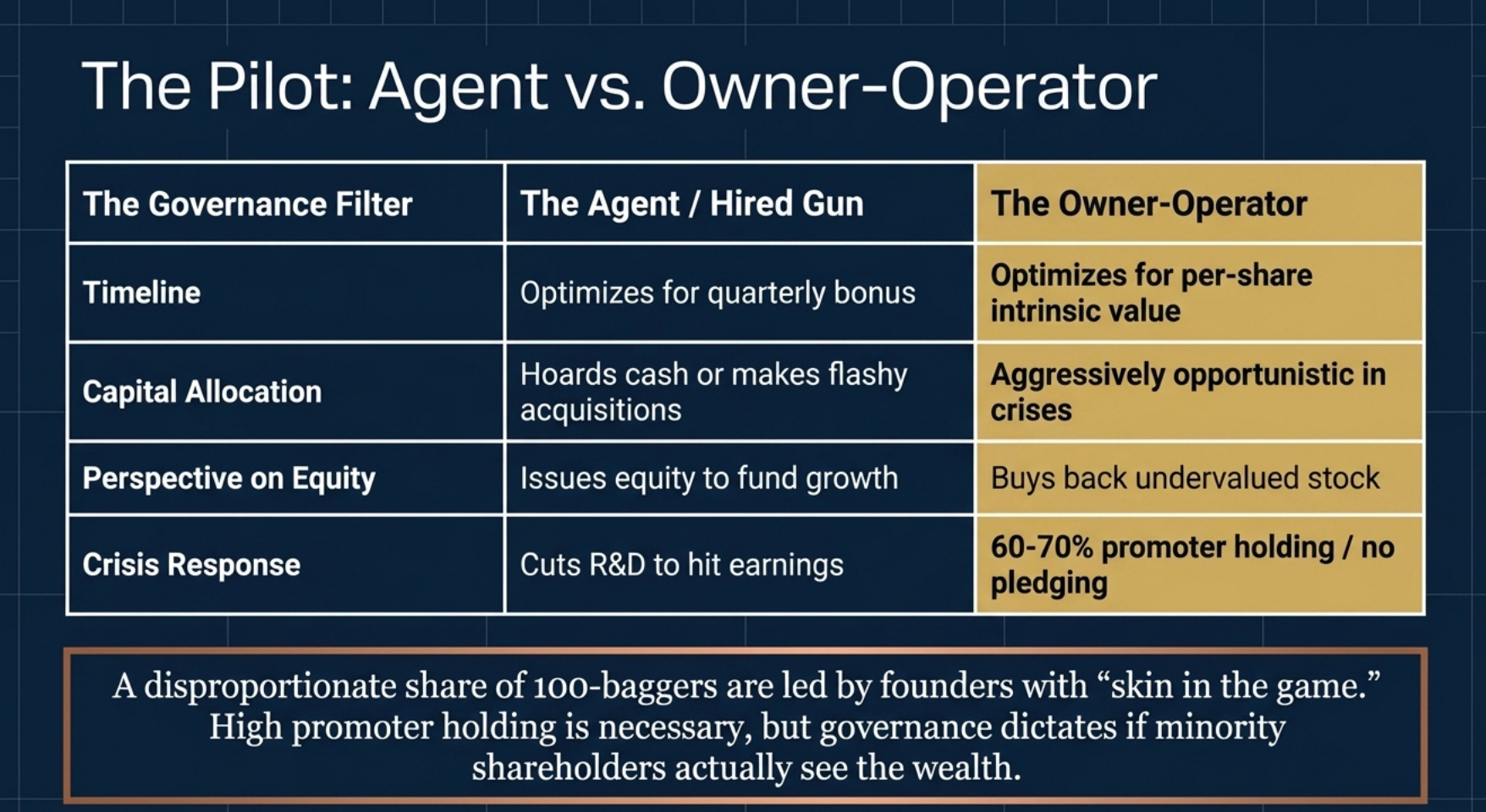

Of all the common traits, this one has the highest predictive power and the least disagreement among serious long-term investors.

Mayer found that a disproportionate share of 100-baggers were led by founders or owner-operators who held significant equity stakes and behaved accordingly. Nassim Taleb frames this precisely as “skin in the game”: when the person making decisions bears the full consequences of those decisions personally and financially, the decision-making quality is structurally different from that of a professional manager optimising for a quarterly bonus cycle.

In India, this manifests through the promoter structure. A promoter holding 60-70% of a growing small-cap company, with no pledging, who has been in the role for fifteen years, who took a modest salary even in difficult years, who has reinvested into the business rather than extracting from it; this is the profile you want. Not because promoters are inherently superior managers. They are not. But because the incentive alignment is real in a way that is genuinely difficult to replicate with professional management.

The corollary, and this is important: high promoter holding is necessary but not sufficient. Indian markets have produced countless promoter-led businesses that destroyed minority shareholder wealth through related-party transactions, capital diversion, or straightforward incompetence. The skin-in-the-game filter must be paired with a governance filter.

Watch what they do with capital. Watch whether their guidance matches their results. Watch whether they buy back shares when the stock is cheap or issue equity when it is expensive. Over five to seven years, these decisions reveal character more reliably than any concall transcript.

The question to ask is simple: does this person act like an owner, or like a well-paid employee of themselves?

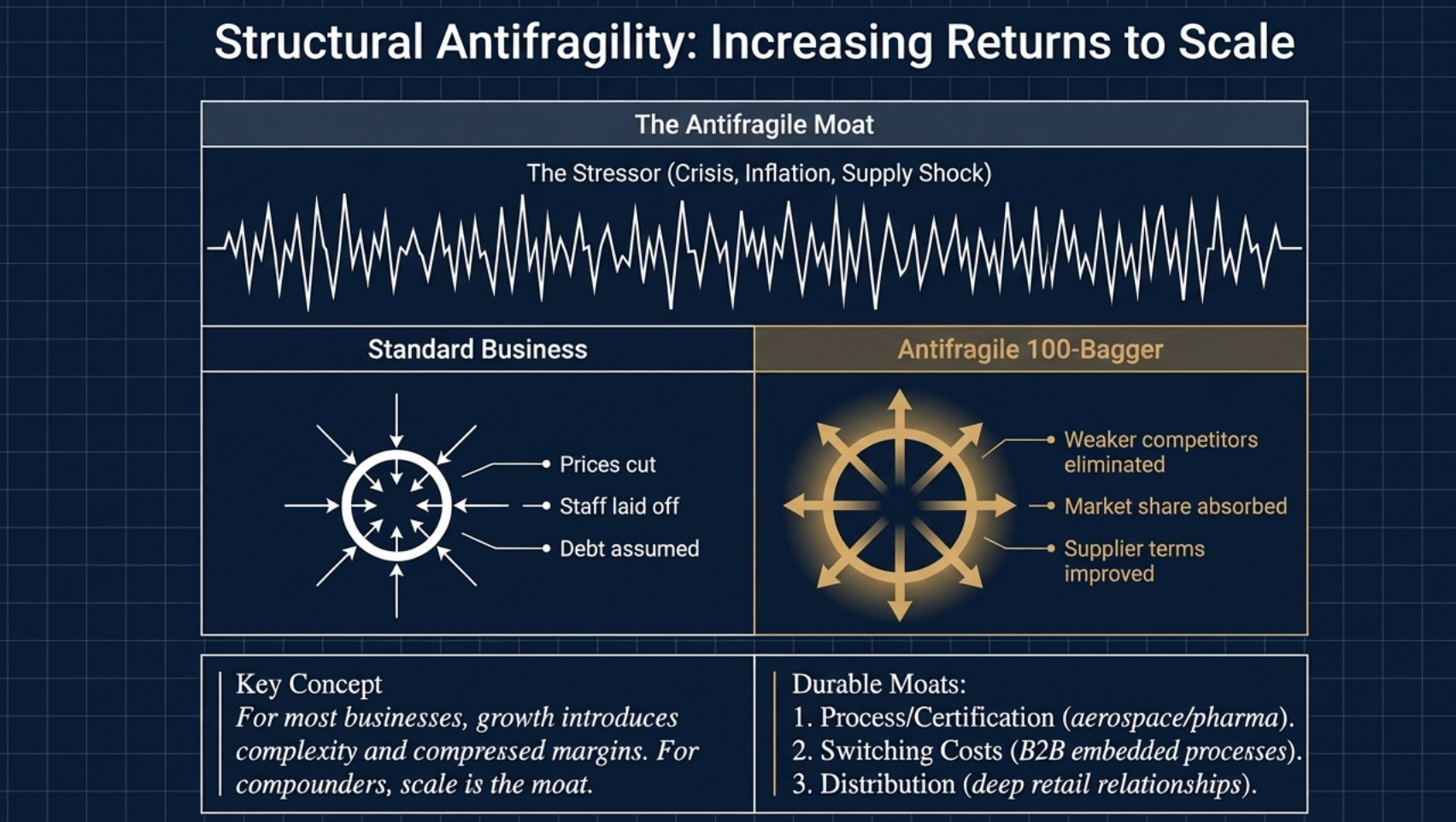

A Business That Gets Stronger with Scale

The businesses that compound the longest are those where the competitive position strengthens, not weakens, as the business grows. This is the concept of increasing returns to scale, and it is rarer than most investors appreciate.

For most businesses, growth introduces complexity and diseconomy. Margins plateau or compress. Competition intensifies. The original advantage dilutes. The business that was exceptional at ₹50 crore revenue becomes merely average at ₹500 crore.

The multi-bagger candidates behave differently. Their moat widens with scale. Think of Pidilite in its early years: every tube of Fevicol sold deepened the brand’s penetration into the carpenter community, which made alternative adhesives harder to sell, which gave Pidilite more leverage with distributors, which expanded shelf access, which sold more Fevicol. The competitive position was self-reinforcing. Scale was not a challenge to manage. It was an engine in itself.

In the Indian small-cap context, this manifests through several types of durable moats.

Process and certification moats are particularly interesting, especially in defence, aerospace, pharmaceuticals, and specialty chemicals. A company that has spent eight years qualifying as a vendor for a defence PSU or an international pharma major has built something that is extraordinarily difficult and time-consuming to replicate. The moat is not the product itself; it is the qualification. A competitor cannot buy their way into it quickly, regardless of capital available.

Switching cost moats appear in industrial B2B businesses where the customer has embedded the supplier’s product into their own manufacturing process. The cost of switching is not just the new supplier’s price; it is requalification, retooling, and the risk of supply chain disruption. These moats are powerful and often invisible to outside observers until you trace the customer relationships carefully.

Distribution moats are underrated in India specifically because of the country’s retail complexity. A company that has spent twenty years building relationships with 40,000 hardware stores or chemist shops across tier-2 and tier-3 India has built something that simply cannot be acquired with capital in any reasonable timeframe.

The test for any moat is a simple but uncomfortable one: if this business were attacked tomorrow by a well-funded, intelligent competitor, how long before customers started leaving? If the honest answer is “many years,” you have something worth understanding deeply.

The Long Runway

High ROCE and a strong moat are wonderful. But without a long runway for reinvestment, the compounding story ends early.

The runway question is simply this: how large is the addressable opportunity relative to the current size of the business? A company with ₹200 crore in revenue in a ₹500 crore total market has very little road ahead. The same business in a market being built by new regulation, demographic change, or import substitution, a market that is ₹50,000 crore and currently fragmented, has decades of growth ahead of it.

India in 2025 is genuinely unusual in the number of structural tailwinds creating new addressable markets almost from scratch. The formalisation of the economy through GST and digital infrastructure is shifting market share from unorganised to organised players at scale across dozens of sectors. The defence indigenisation mandate is creating captive demand for Indian manufacturers who could not previously access these customers. The China+1 shift in global supply chains is expanding the addressable market for Indian chemical, electronic, and pharmaceutical manufacturers.

In each of these cases, the runway is long, and early movers with the right capabilities will compound for years before saturation becomes a genuine constraint. The investor’s job is to identify these runways before they are obvious, which brings us to size.

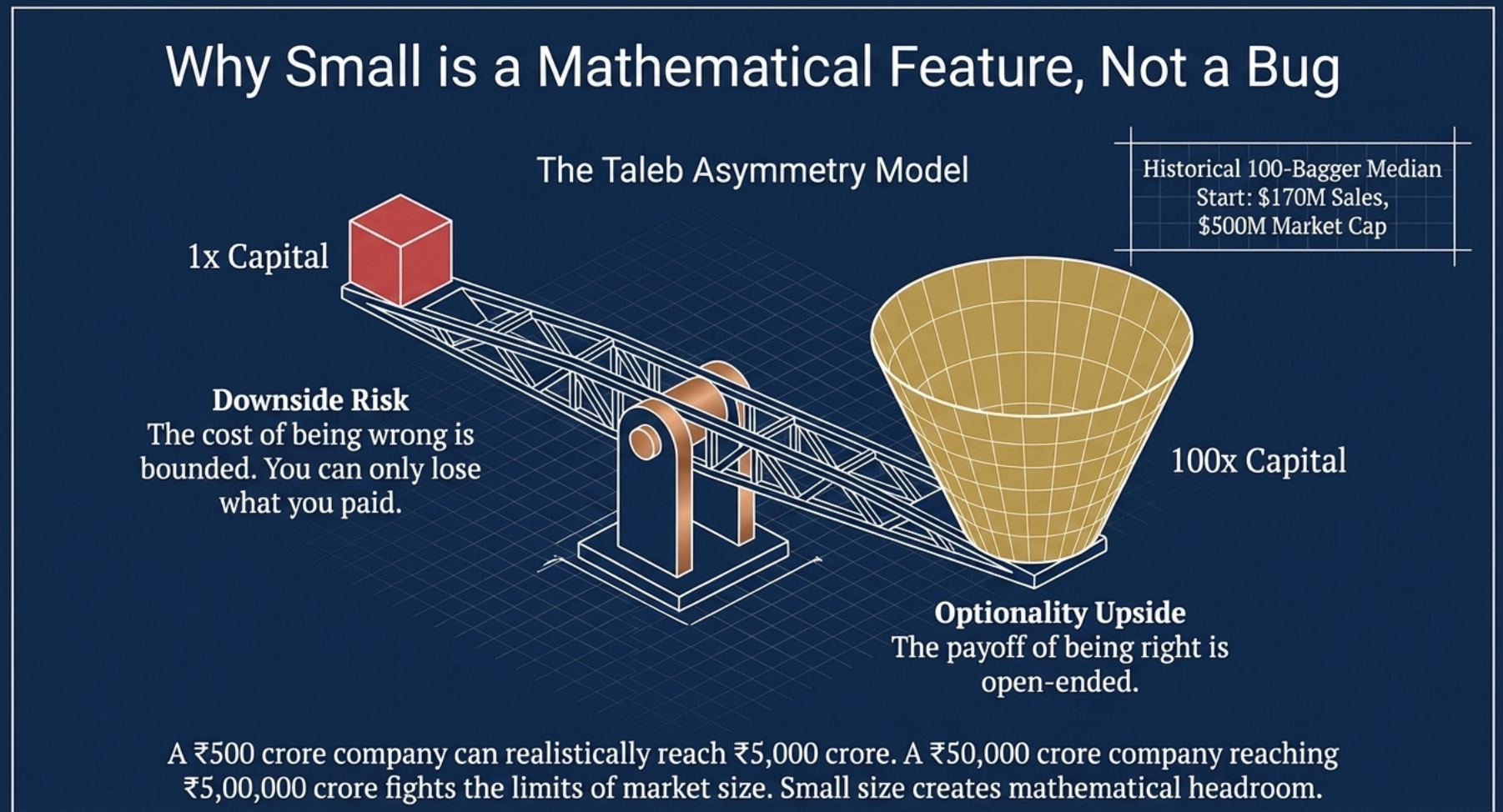

Small Is a Feature, Not a Bug

This is perhaps the most counterintuitive insight in the study of multi-baggers, and it deserves stating plainly.

For a company to 10x in market capitalisation, it needs to go from, say, ₹500 crore to ₹5,000 crore. That is achievable. For a company already at ₹50,000 crore to 10x, it needs to reach ₹5,00,000 crore. The base rate for that happening is constrained simply by the absolute numbers; the business would have to capture an unrealistically large share of its market, or expand into multiple new markets, all successfully.

Small size creates mathematical headroom for extraordinary returns. It is not sufficient on its own; thousands of small, cheap, poorly run businesses will stay small and poorly run indefinitely. But for a quality business with a strong moat, an owner-operator, and a long runway, small size is the accelerant.

The investor willing to be patient in the early, illiquid, under-researched stage of a company’s life has a genuinely structural advantage: you can get in at prices that are unavailable once the business becomes large enough to attract institutional attention, analyst coverage, and index inclusion. Your constraint, meaning smaller capital, no redemption pressure, no career risk, is your edge. Use it.

The Taleb Lens: Optionality and Antifragility

Most investment frameworks treat the future as a probability distribution centred around an expected value. You estimate what a business will earn in five years, apply a multiple, discount back, and compare it to today’s price.

Nassim Taleb’s work suggests a very different way of thinking about the kind of asymmetric opportunities that genuine multi-baggers represent.

The first concept is optionality. An option, in its pure form, has a defined and bounded downside; you can only lose what you paid, and a theoretically large upside. Taleb argues that investors should seek situations where the payoff profile resembles this structure: where the cost of being wrong is small and bounded, and the payoff of being right is large and open-ended.

Many small-cap businesses in India have exactly this profile. If you invest in a ₹400 crore market cap business at a sensible valuation and you are wrong, the moat does not hold, management disappoints, the sector headwind is stronger than anticipated, you might lose 40-50% of your capital over several years. That is painful but survivable with sensible position sizing. If you are right, and the business compounds at 25% for fifteen years, your return is 20-25x. The asymmetry is extreme.

The practical implication of thinking in options is that you are not trying to be right on every position. You are constructing a portfolio where many positions will underperform, a handful will meet expectations, and one or two will deliver extraordinary returns that more than compensate for everything else. The Kelly criterion, applied thoughtfully, suggests that when you have a significant edge and extreme asymmetry, you should be concentrated: not reckless, but meaningfully positioned. A 1% position in your best idea, sized as though you might be wrong about it, is usually not how great wealth is built.

The second concept is antifragility. Taleb distinguishes between things that break under stress (fragile), things that resist stress (robust), and things that actually improve under stress (antifragile). The best businesses in the world are antifragile; economic disruptions, competitive attacks, and supply chain crises make them stronger, not weaker.

How? Because crises eliminate weaker competitors, deepen the moat of the survivor, and often create acquisition or talent recruitment opportunities at distressed prices. The company with a strong balance sheet, no debt, and a sticky customer base that navigates a sector downturn emerges on the other side with more market share, better supplier terms, and a more durable competitive position than before the crisis.

When screening for multi-baggers, pay close attention to how a company behaved in the last significant downturn. Did it cut prices to defend revenue? Lay off core engineering or sales staff? Take on debt to survive? Or did it hold margins, retain key people, and emerge larger? The answer tells you whether you are looking at a fragile business dressed up in a good-looking income statement, or a genuinely antifragile one.

The FY20-21 Covid period and the FY22-24 input cost inflation cycle were both excellent stress tests in the Indian market. The businesses that navigated both while compounding their competitive position are worth understanding very carefully. The ones that stumbled and rationalised it afterwards are worth approaching with scepticism, regardless of how good the story sounds today.

The Maths of How a 10-Bagger Actually Happens

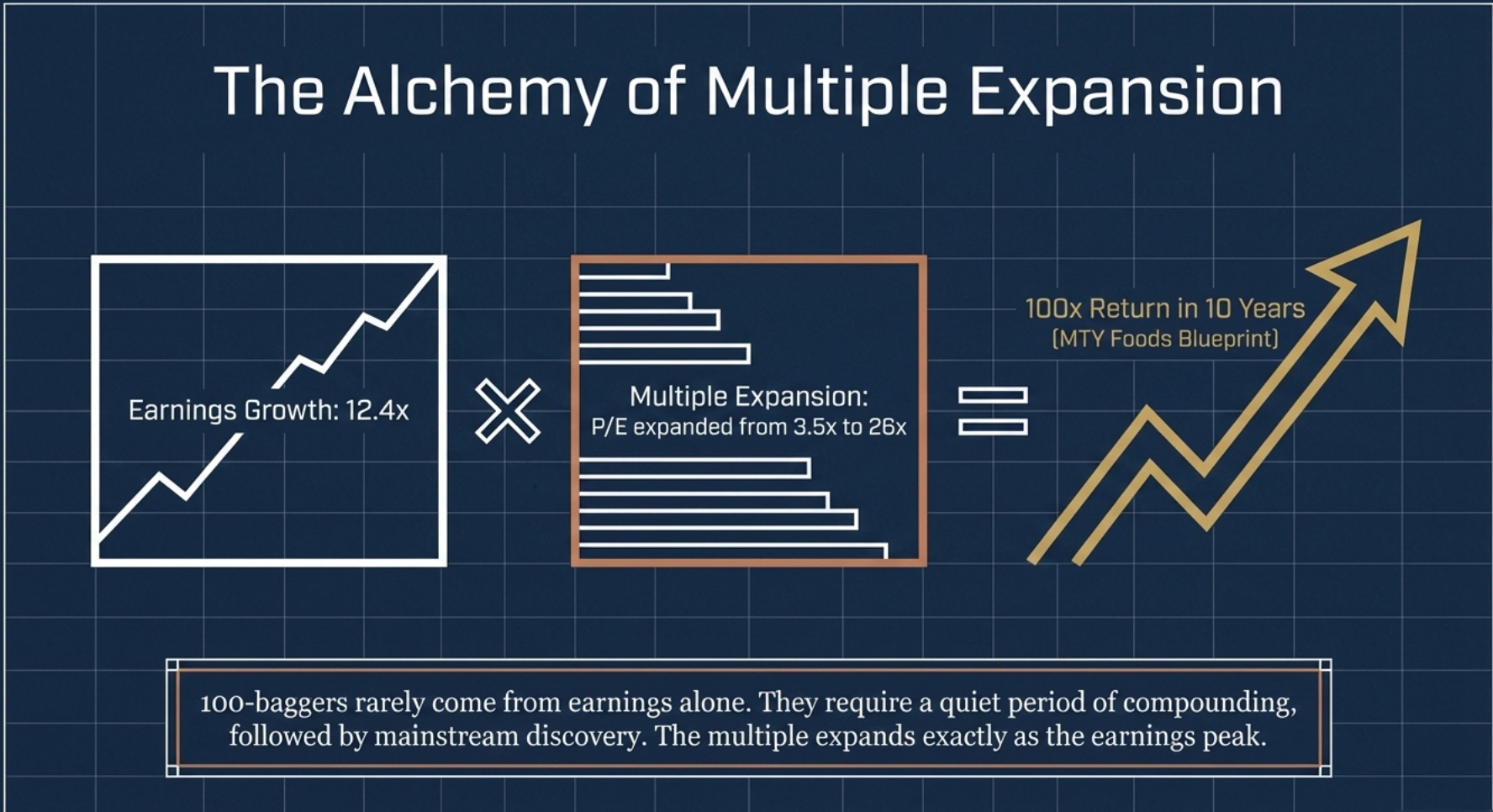

A 10x return in a stock does not come from one source. It comes from two working together: earnings growth and multiple expansion.

Consider a business earning ₹10 crore in PAT, trading at 15x earnings; a market cap of ₹150 crore. If it grows earnings 5x to ₹50 crore over ten years, and the market re-rates it from 15x to 30x as the business becomes better understood and attracts more capital, the market cap moves to ₹1,500 crore: exactly a 10x return.

This decomposition is important because it tells you that valuation expansion is a meaningful part of the journey, not a nice-to-have. And valuation expansion in a growing business is not arbitrary; it is the natural result of the twin engines becoming visible to a wider audience.

Here is what typically happens: a business compounds quietly for several years. Revenue grows, margins expand, ROCE climbs. The stock does very little because nobody is paying attention. Then something changes: an analyst initiates coverage, a mutual fund takes a meaningful position, the sector narrative enters mainstream financial media, or the company simply becomes too large to ignore. Suddenly, capital that was unavailable to the stock at a ₹300 crore market cap is available at ₹800 crore. The same fundamental business, the same ROCE, the same growth rate, but now there is a buyer on every dip, and the multiple expands.

Mayer’s research on 100-baggers showed that the combination of consistent earnings growth and gradual multiple expansion is the dominant pattern. Very few multi-baggers came from a sudden earnings explosion or a single re-rating event. Most were years of quiet compounding that looked unremarkable from the outside, punctuated by the eventual discovery by a wider investment community.

The practical implication: do not wait for the re-rating to begin before taking a position. By then, the easy money has been made. The investor who benefits most is the one who identified the twin engines running, high ROCE plus high reinvestment rate, before the broader market arrived.

The Behavioural Nightmare of Riding Winners

Now comes the hard part. The part that destroys most of the returns that good fundamental analysis should generate.

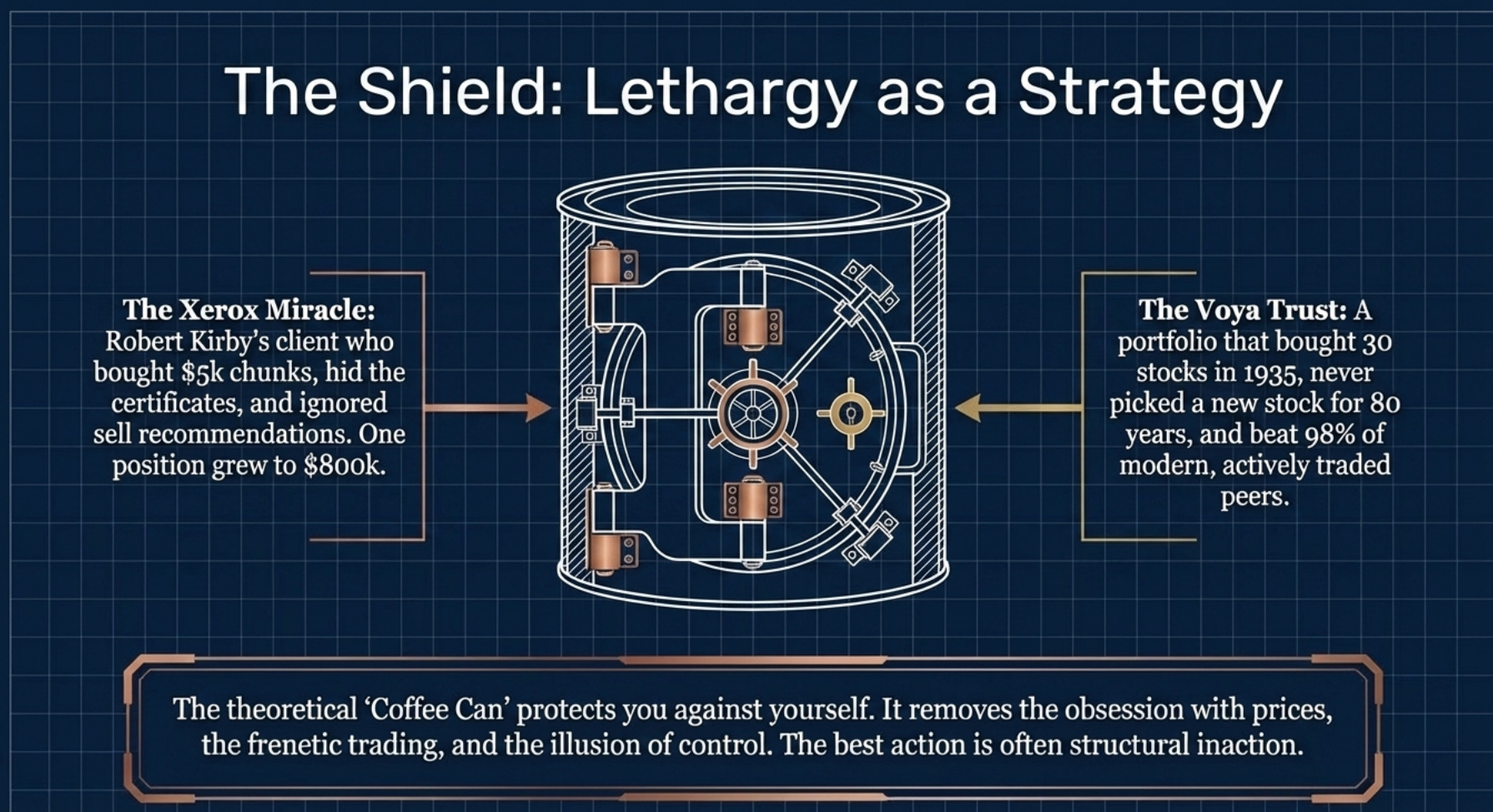

Charlie Munger, in his famous USC commencement speech, talked about the value of “sitting on your ass” as a core investment activity. He was not being glib. The ability to do nothing, when every instinct, every news headline, every dinner party conversation is telling you to act, is one of the most valuable and rarest skills in investing.

The research on multi-baggers is humbling on this point. Mayer found that many of his 100-bagger stocks corrected 50% or more at least once on the journey to 100x. Many corrected more than once. The investors who captured the full return were not those who timed these corrections perfectly. They were those who held through them.

Why is this so difficult? Because human psychology is wired for exactly the wrong behaviour in this situation.

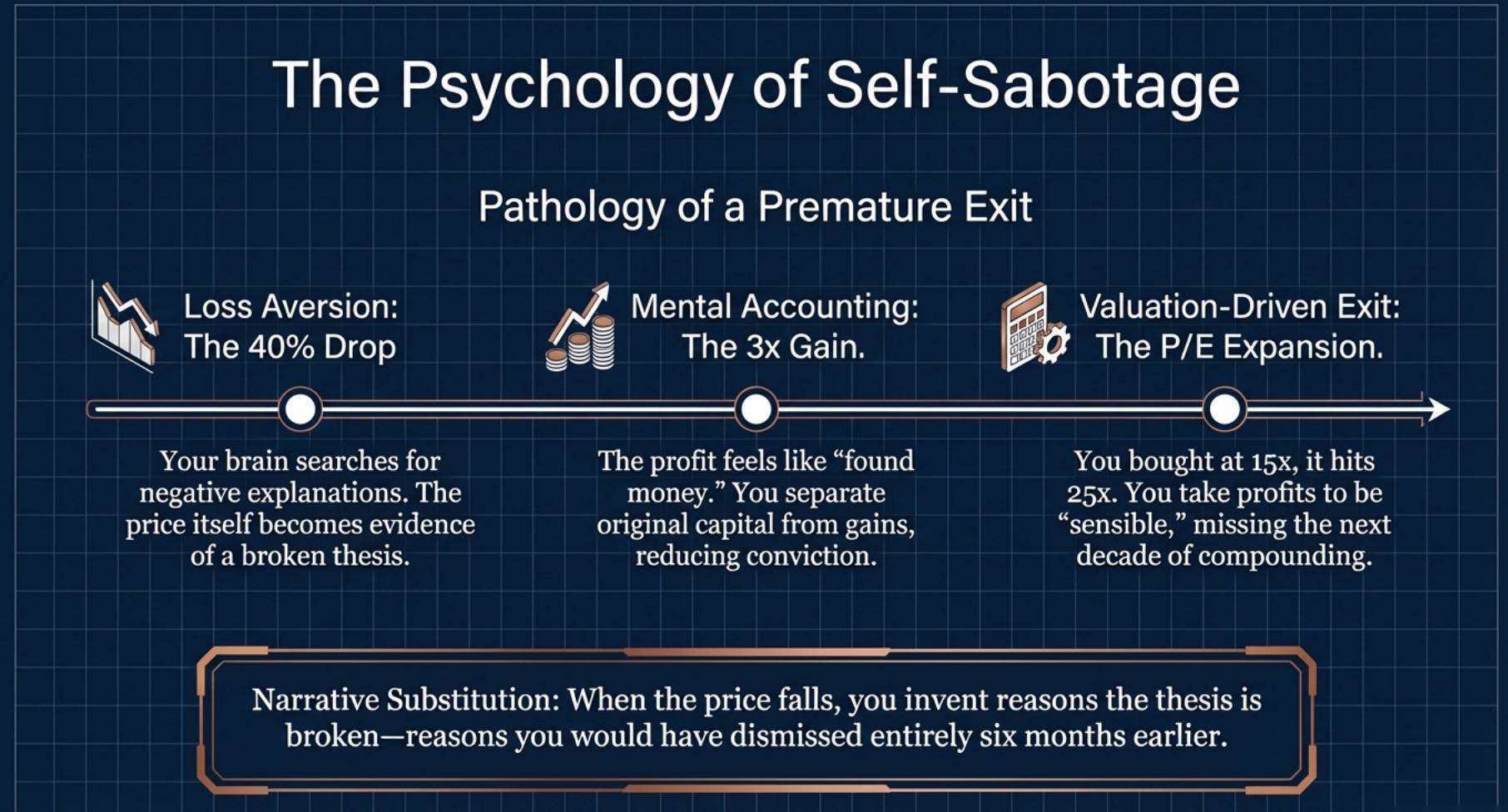

Loss aversion means the pain of watching a position fall 40% is felt more acutely than the pleasure of watching it rise 40%. The evolutionary logic is sound; our ancestors survived by avoiding threats. But in the context of long-term investing, this bias is ruinous. It makes you sell excellent businesses at precisely the worst moment.

Mental accounting means that once a stock has tripled, you have mentally separated the “original capital” from the “profits.” The profits feel like found money, and found money feels fine to risk or protect. The dangerous implication is that you are more likely to sell a stock that has tripled than to hold it, not because your analysis has changed, but because the psychological accounting has shifted.

Narrative substitution is perhaps the most insidious. When a stock corrects sharply, your brain automatically searches for a negative explanation. The price itself becomes evidence of a fundamental problem. You start finding reasons the thesis might be broken, reasons you would have dismissed entirely six months earlier when the stock was rising. The price change does not change the fundamentals; it changes the story you tell yourself about the fundamentals. This is the trap.

The valuation-driven exit is the most common form of self-sabotage for investors who think of themselves as disciplined. You bought at 15x earnings. The stock doubles and now trades at 25x. You tell yourself it is expensive and you should take profits. The business then compounds earnings for five more years, the multiple stays elevated as the quality becomes widely recognised, and you watch from the sidelines. The error here is treating valuation as a static measure when what matters is whether the business is growing its intrinsic value fast enough to justify the current multiple, and whether that growth has years of runway remaining.

Munger’s antidote to all of this is characteristically blunt. He called it “the discipline to do nothing when doing nothing is the right answer.” More specifically, he argued that a serious investor would have very few truly great ideas over an investing lifetime, perhaps five to ten genuinely exceptional businesses, and that the behaviour which destroys most investors is not bad stock-picking but good stock-selling.

The practical antidote is one Mayer also recommends: write down the thesis before you invest. Every key assumption. Every reason you believe the moat is real. Every metric you will monitor. Then, when the stock corrects 35% in a market downturn, you do not ask “why is the price falling?” You ask: “Has anything in my thesis actually changed?” If the ROCE is intact, the promoter has not reduced his stake, the order book is growing, and the moat looks as durable as it did at purchase, the price is noise, not signal.

Hold the businesses where the facts support the thesis. Revisit, genuinely revisit and not panic-sell, the ones where the facts have shifted.

What Munger’s Inversion Tells Us About Failure

Charlie Munger borrowed his favourite mental model from the mathematician Carl Jacobi, who said: “Invert, always invert.” Instead of asking how to succeed at something, ask what all the ways of failing look like, and then avoid those things systematically.

Applied to multi-bagger investing: instead of asking what makes a 10-bagger, ask what destroys a potential 10-bagger before it gets there. The answers are instructive.

Premature diversification is perhaps the most socially acceptable form of return destruction. You have twelve stocks. Two of them are genuinely exceptional. Ten of them are fine. Over time, you keep adding new positions, diluting the allocation to your best ideas. Buffett’s answer to this was radical concentration; he has repeatedly said that most investors would be better served by a “twenty punches” rule, where you only get twenty investment decisions in your lifetime and had better be sure before using one. The spirit of this, applied practically, is that a 2% position in your highest-conviction idea is an admission that you do not really believe in it.

Governance deterioration is a real and specific risk in the Indian small-cap context. Many promoter-led businesses are excellent at the early stage; the promoter is hungry, focused, and aligned with minority shareholders. As the business grows and the promoter becomes wealthy, incentives can shift. Related-party transactions increase quietly. Salary extraction grows. Capital allocation quality falls. The best protection against this is early detection: watch for changes in auditor, rising promoter remuneration relative to profits, increasing related-party revenue as a percentage of total revenue, and changes in board composition that reduce independent oversight.

Sector disruption is the moat you identified becoming structurally irrelevant. The best protection is to regularly re-examine whether the source of competitive advantage is still intact in a world that looks meaningfully different from when you invested. A distribution moat in a category moving rapidly to e-commerce is worth much less than it was five years ago. A process moat in a chemistry being replaced by biotech is eroding. The thesis is not a static document; it is a living framework that should be revisited with fresh eyes at least annually.

Balance sheet fragility deserves particular respect. A business with a strong franchise but too much debt on the balance sheet can be permanently impaired by a temporary downturn that an unleveraged version of itself would have navigated easily. Taleb’s point applies directly here: in a world of unpredictable shocks, a pandemic, a sudden commodity spike, a regulatory reversal, the clean balance sheet is insurance. Do not undervalue it at the point of investment.

Anchoring to the peak price is a behavioural trap that affects even experienced investors. Once a multi-bagger has run significantly and then corrected from its peak, many investors sell at “only” 5x when they could have held to 10x, simply because 5x feels disappointing relative to the peak. The peak price is entirely irrelevant. The only question that matters is whether the underlying business will be worth meaningfully more in five years than it is worth today.

A Practical Screening Framework

Given everything above, here is a condensed framework for identifying 10-bagger candidates in the Indian small and micro-cap universe.

Start with the financial fingerprint. ROCE consistently above 20%, and ideally on an upward trajectory. Revenue and PAT both growing above 20% per annum over the last three to five years. Free cash flow conversion above 60% (CFO to EBITDA). Net debt-to-EBITDA below 1.5x and declining. No significant related-party transactions or promoter pledging.

These are elimination filters, not targets. You are looking for businesses where all of these conditions hold simultaneously, which narrows the field dramatically.

Then look for the runway. Is the addressable market large relative to current revenue? Is there a structural tailwind, regulatory, macroeconomic, or demographic, that is newly created or newly accelerating? Is the company gaining share from less capable or less organised competitors?

Then assess the moat. What specifically makes this business difficult to replicate? Has the competitive advantage held up under past stress? Is the position strengthening or weakening as the business scales?

Then study the management. Listen to every concall from the last eight quarters and track guidance against delivery. Watch capital allocation decisions over a long period. Look for the owner-operator mentality in how they speak, where they spend, and how they treat minority shareholders.

Then think about the twin engines. What is the current ROCE? Is it expanding? And critically: does the business have a large enough reinvestment opportunity to keep deploying capital at these rates? The answer to this last question determines how long the compounding can run.

The One Thing Nobody Tells You

Here is the truth about 10-baggers that most content on this subject quietly avoids.

Most investors who hold a 10-bagger do not make 10x. They make 3x. They make 4x. They sell somewhere along the way for entirely rational-sounding reasons: it looks expensive, they need the cash, something else looks more interesting. And they watch the rest of the journey unfold from the sidelines.

The analysis, the screening, the moat assessment, and the financial modelling are the relatively easy parts. It is cognitively demanding but emotionally neutral. You are working with data, not with capital that has a psychological cost attached to it.

Holding is different. Holding requires you to repeatedly resist the urge to act when acting feels necessary and intelligent. It requires you to watch the price fall 40% and conclude, based on your own judgement rather than the market’s, that the business is fine. It requires you to look at a 5x gain and override the voice telling you to protect it.

Munger described this as being “comfortable with inaction in the presence of apparent opportunity.” The paradox is that the most valuable action in portfolio management, the one that captures the truly extraordinary returns, often looks identical to laziness from the outside.

The investors who made 100x in Wipro, Page Industries, Eicher Motors, or Bajaj Finance did not have better research than everyone else. They had research that was good enough to establish conviction, combined with the psychological durability to hold through every single moment when selling felt like the sensible, prudent, grown-up thing to do.

That is the real 10-bagger framework. And the hardest part of it cannot be learned from a book or a Substack post. It can only be earned through the long, uncomfortable, frequently humbling practice of staying the course when everything around you suggests otherwise.

What I Am Watching

For those who want to apply this framework practically, here are the specific metrics I track as ongoing signals that a potential compounder remains on track.

ROCE trajectory: Is it expanding, stable, or compressing? Expansion signals that the competitive position is strengthening. Compression demands investigation before any other analysis.

Reinvestment rate: What fraction of earnings is the company redeploying into the business? Is new capex going into proven, high-return business lines or into speculative adjacencies?

Promoter behaviour: Buying at market prices or reducing? Any new pledging? Any changes in related-party structures or board composition?

Working capital cycle: Is it stable or deteriorating? Worsening debtor days in particular can be an early signal of revenue quality issues that will only appear in the cash flow statement quarters later.

Guidance versus delivery: Track this over four to six consecutive quarters. Consistent over-delivery on guidance is one of the strongest available signals of both management quality and underlying business momentum.

The businesses genuinely compounding will show stability or improvement across most of these metrics, most of the time. The ones where two or three metrics start deteriorating together deserve a hard, unsentimentally honest look at whether the thesis is still intact.

The patience to tell the difference, and to act accordingly, is the entire game.

I asked Notebook LM to make a video for me on this topic: Watch it here-

Disclaimer: I am a SEBI-registered Research Analyst (Registration No. INH000023807). This piece is educational and analytical in nature and does not constitute investment advice. I may hold positions in companies referenced in my broader research. Please conduct your own due diligence or consult a qualified financial adviser before making any investment decisions.

Valuable information. Very well explained.

Absolute gem 💎🤌🏻🙌🏻